An opportunity for a potential world-class nickel discovery is hidden away in one of Canada’s best Nickel development companies FPX Nickel Corp. (TSXV:FPX; OTC:FPOCF). FPX Nickel is primarily known for its PEA-stage Baptiste nickel deposit in its 100%-owned Decar nickel district in British Columbia. But CEO Martin Turenne shares in this interview that he does not believe the market has realized the Decar nickel district’s massive exploration potential which is about to be drilled this year.

FPX Nickel will begin this summer the first ever drill program at its Van target. Martin shares regarding Van’s prospectivity: “Most notably at the Van target, where we have delineated a drill target there based on outcropping surface samples of bedrock that covers an area about three square kilometers of outcrop. So that is the target scale. By way of comparison, the lateral footprint of Baptiste is only about two and a half square kilometers. And the other thing that we see at Van is not only is it larger in its scale conceptually at surface than Baptiste, but the grades are higher. The grades are about 10% to 15% higher in surface samples (0.16% DTR Ni).”

Click Here to Listen to the Audio

Sign up (on the right side) for the free weekly newsletter.

0:00 Introduction

1:40 Bullish on nickel

4:49 Baptiste world-class nickel deposit at Decar project in BC

7:30 FPX Nickel future upside after nice share price run

9:12 Why Baptiste’s metallurgy is so important

10:54 Baptiste’s “clean nickel” appeals to majors & investors

13:18 Is FPX Nickel only a leverage play on nickel prices?

14:47 Baptiste’s CAPEX relative to other nickel projects

16:23 Van target is a potential world-class nickel discovery

18:22 “Nickel discoveries always do well because of their rarity”

20:22 Share structure with no warrant overhang

22:14 Treasury and burn rate

23:22 Upcoming catalysts in 2021

FPX Nickel’s Corporate Presentation

TRANSCRIPT:

Bill Powers: Let’s talk about the nickel market. Give us a thumbnail overview of why you’re bullish on nickel.

Martin Turenne: Sure. So just in terms of nickel use, so the main drivers of nickel demand are stainless steel, which is a function of industrial activity and consumer retail demand. And the fastest growing segment of nickel demand is nickel being used in electric vehicle batteries. So, the nickel market to date has… There’s only been about 3% or 4% of total demand from the battery sector, but that’s projected to go to about 20% to 25% of overall nickel demand over the next decade. And so we’re going to have to add a significant amount of new capacity to nickel supply in order to meet that demand from the battery sector. And so, one of the other trends that we see is increasing use of nickel in each EV battery because it helps the batteries maintain a charge longer and thus extend the range of the cars. So the future is certainly bright for nickel coming from its traditional uses in stainless, but then especially from that supercharging of demand from the EV story.

Bill: I remember in our first interview back in October of 2018, you actually said in that interview that even if there was an increase from demand from the EV revolution, you still see a rising nickel price, right?

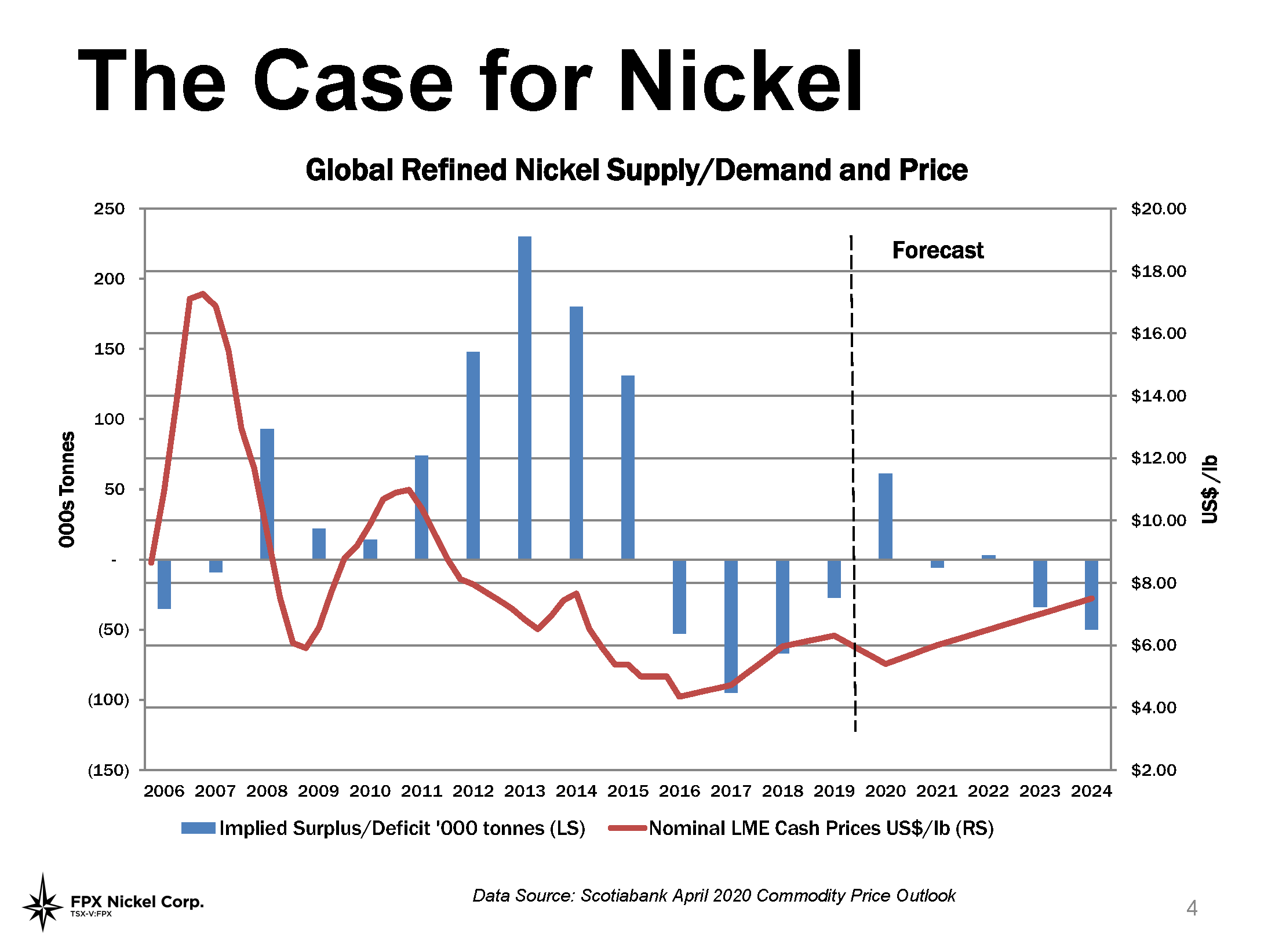

Martin: That’s correct. So the nickel market between 2016 and 2019 had developed a period of long-term structural deficit. That means that the supply was not high enough to keep up with demand. And during that period of time, EV demand was just a blip on the radar. And so you still have a nickel market here that faces long-term structural shortfall of supply for the main uses being stainless steel. And so adding in additional demand from effectively a brand new source of EV batteries is sort of the cherry on top. And it certainly presents the risk, if anything of the nickel price running too high, too fast going forward.

Bill: And where does the nickel price stand today relative to some of the past peak cycles?

Martin: I think the most relevant peak cycle to consider certainly in the 21st century was related to the commodity super cycle, the Chinese-driven commodity super cycle in the 2005 to 2008 period. The nickel price at that time on a spot basis rose to about $24 a pound. It subsequently went down to a low of around $3.60 a pound. And it now sits at about $8 a pound. So at about one third of what it was in the previous peak. $8 a pound is roughly, if you look back over the last 40 years, it’s about what the inflation adjusted average nickel price has been over that span of time, maybe just a little bit higher. And so at today’s level, we’re at sort of historical average levels, but still well below what we’ve seen in previous peaks.

Bill: Let’s discuss your company, FPX Nickel. So the main value driver is the Decar project and specifically the Baptiste deposit there, which is at the PEA stage. Give us an overview of your project, please?

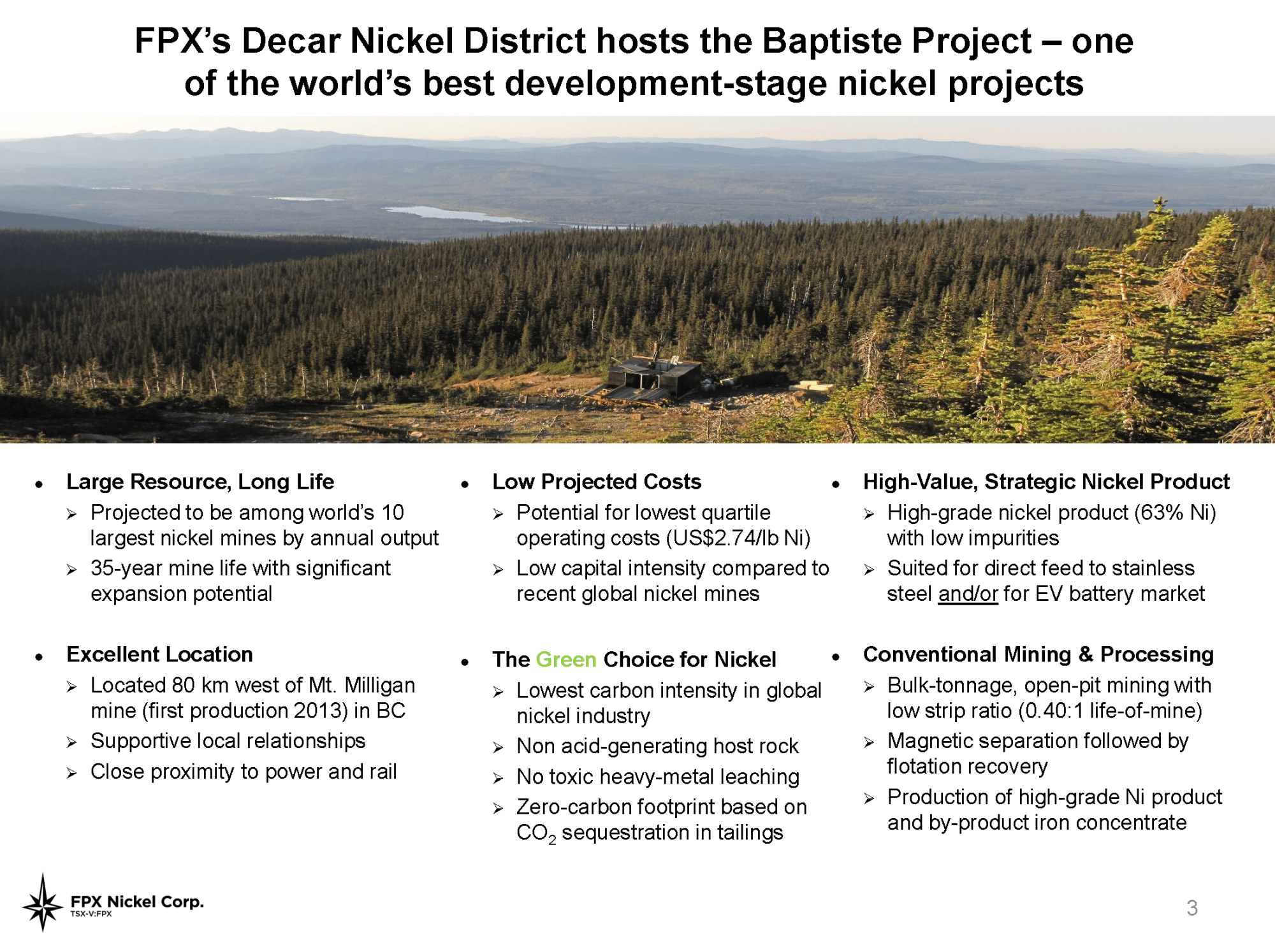

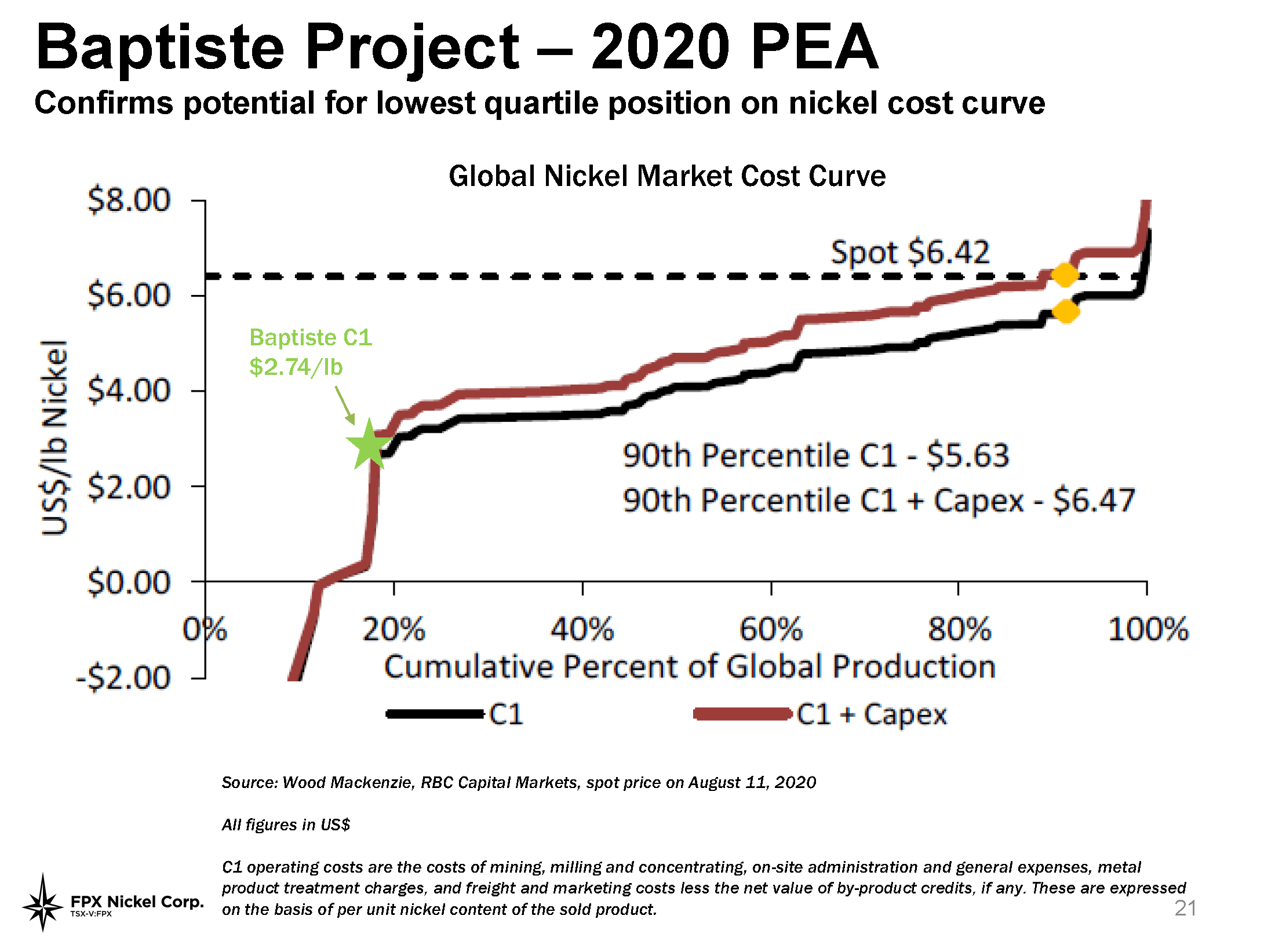

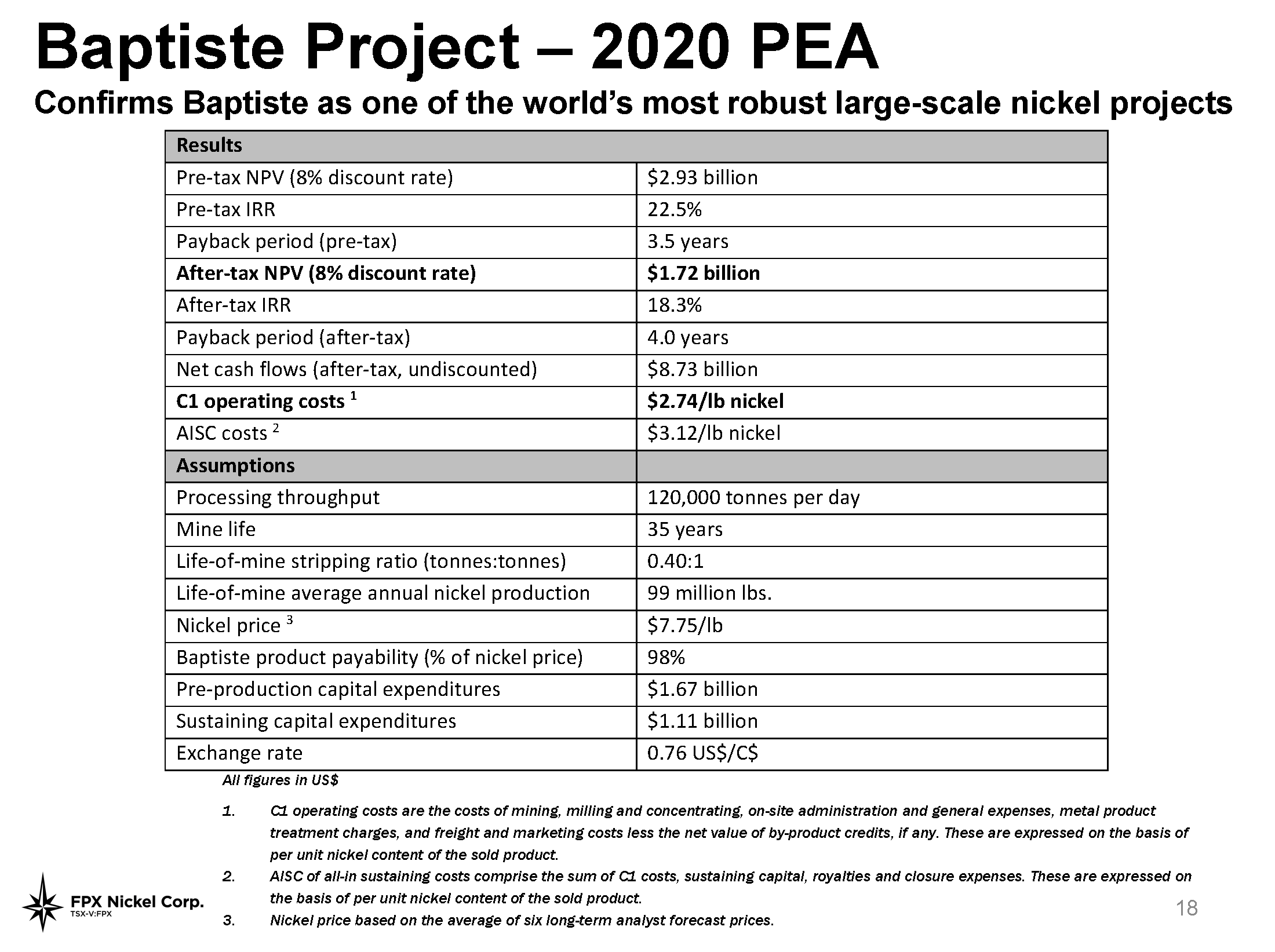

Martin: We own 100% of the Decar Nickel District located in central British Columbia in an area that’s well known for very large multi-generational mines and mineral deposits. Decar as you noted hosts a very large nickel deposit called Baptiste. Baptiste stands is one of the largest, in fact, one of the 10 largest nickel deposits in the world as of today. So we recently completed a preliminary economic assessment or PEA on Baptiste that shows that it could have a very long mine life, multi-generational at 35 years, produce around 100 million pounds of nickel every year over that span, which would make it one of the 10 largest nickel mines in the world. And produce at a very low cost C1 operating costs below $3 a pound, which would put us in the bottom quartile of the cost curve. So while we are junior company, we do think that ultimately this is the type of project that will sit in the hands of a major company and be sort of a multi-cycle, multi-generational, sort of powerhouse nickel producer.

Bill: So that is the exit strategy, ultimately is to sell to a major producer?

Martin: I think a major or there are other potential project partnerships or project exit partners. What we’re seeing, I think that’s quite interesting right now is battery makers and automakers are really having to think about security of supply of nickel units. And also trying to think about having some degree of cost certainty on the nickel inputs in their batteries. And the batteries are one of the most important or costly pieces of a Tesla or any other EV. And so being beholden to kind of commodity price volatility is inherently a risk for battery makers and car makers. And so what we’ve started to is those groups, particularly on the battery side, starting to make upstream investments in mining projects, specifically in nickel projects at a relatively early stage in order to kind of get a pole position to secure supply and to secure those units at a cost that they can then plan their businesses around.

So what that does for a company like us is it really expands the range of potential partners or exit strategies to include of course, the major mining companies, but also to think about sort of downstream users who might look at making upstream investments in mines.

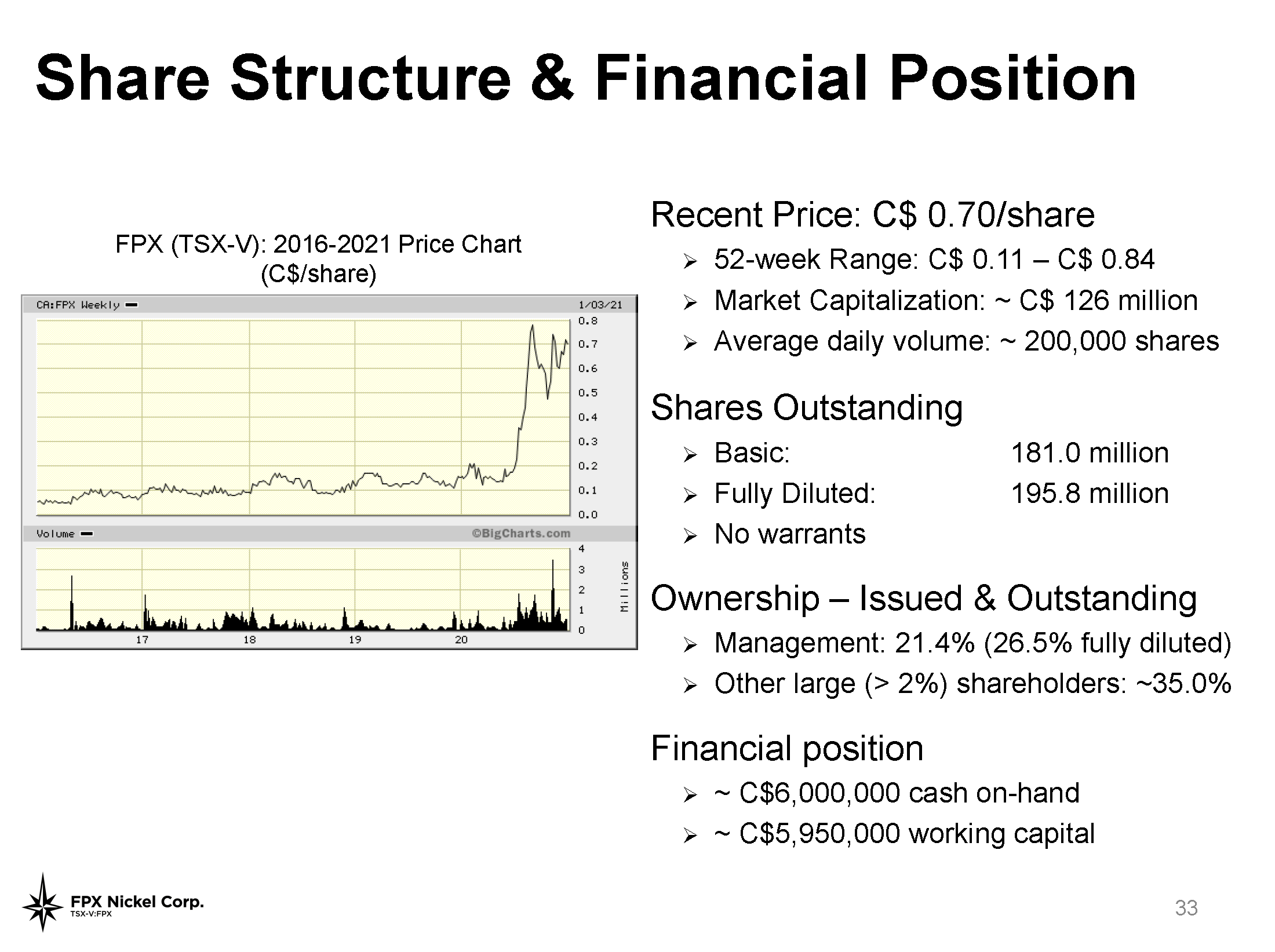

Bill: Your company has had a lot of positive attention since the summer of 2020. I remember when we first met your share price was about 9 cents Canadian and it’s been trading in the 60 cent range, they’re up 60 to 70 cent range Canadian. So, it’s had a nice run. So when investors are looking at it and saying, “Oh, I missed the boat on this one.” What would you say to those that feel like you already had your run?

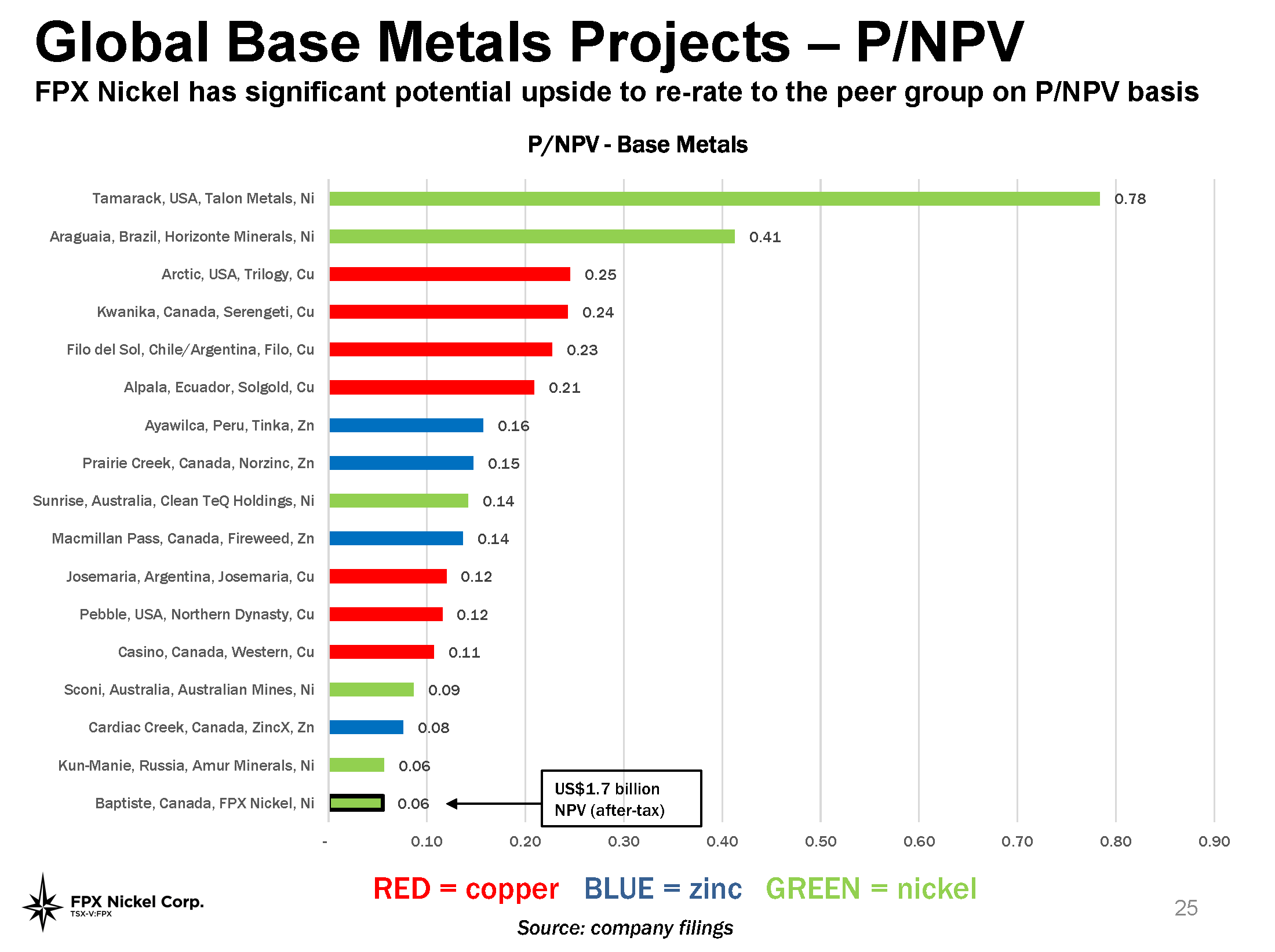

Martin: Yeah, a good question. And one that we get all the time. I’d say we’d just look at kind of valuation in the peer group as a starting point. So the PEA that we just completed showed a net present value on a Canadian dollar basis after tax of, in excess of 2 billion Canadian dollars. And we currently have a market cap of around just over 100 million Canadian dollars. So we trade at about 5% of our project value in our study. Typically base metal projects at this stage of development in the PEA to PFS stage, they often will trade at 15% to 20% of their project value. And so, this has been a very underpromoted, undermarketed, underknown story for many years. And what we saw last year was the dawning of people coming to realize the story. We got research coverage from a couple of banks. And so we see that simply getting a rerate to the peer group is one way to get that value. But beyond that, we have a kind of very sort of dense year ahead of us in terms of activities and news flow.

And those are the things that I think are going to help to one, de-risk and advance the project and add value to it, and two also provide the type of news flow that can get people’s attention.

Bill: So one of the things you did in your PEA was look at metallurgical studies. I remember talking to you 18 months ago or so at a conference and you were focused on metallurgy. Talk about why for nickel projects, it’s so important that you get your metallurgy right?

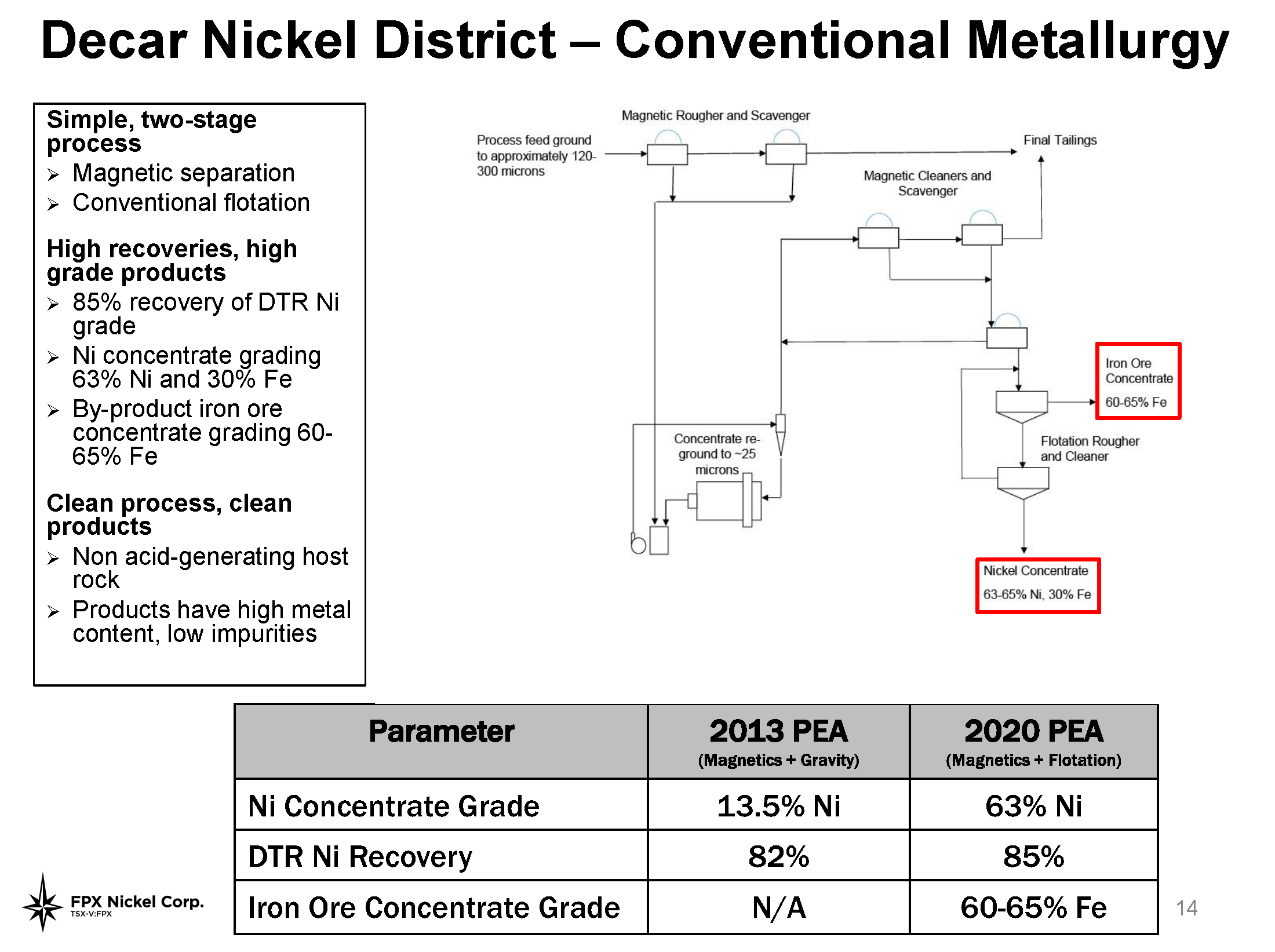

Martin: Metallurgy is fundamental to putting together kind of a profitable mining operation. A lot of people are really focused on head grade within the mineral deposits, and of course that’s very important. But what we find in a lot of nickel deposits is that you might find deposits that have attractive head grades, but the recoveries are quite low, or the recoveries accomplished even at that low level using very complicated, very expensive technologies. And in some cases, sort of quasi-experimental technologies. So one of the advantages of our project here is the very high rates of recovery that we can achieve using very simple, and I should also add very clean processes to recover nickel into a very high value product. And that is a product that can be sold directly to end users.

What you find in most base metals is that mining companies will produce a concentrate, whether it’s a copper concentrate, a nickel concentrate, or a zinc concentrate, and if they’re not integrated, if they don’t have their own smelters, they have to sell to smelters and accept fairly punishing payment terms. The advantage we have with our deposit, which we’ve shown in our metallurgical testwork that you alluded to, is the ability to produce an end product that goes directly to end customers. We cut out that smelter middleman, and that means we get paid a lot more for our product versus the peer group.

Bill: And there’s also an appeal there to any company that might work with you or buy you eventually, right? Because it’s lower carbon emissions?

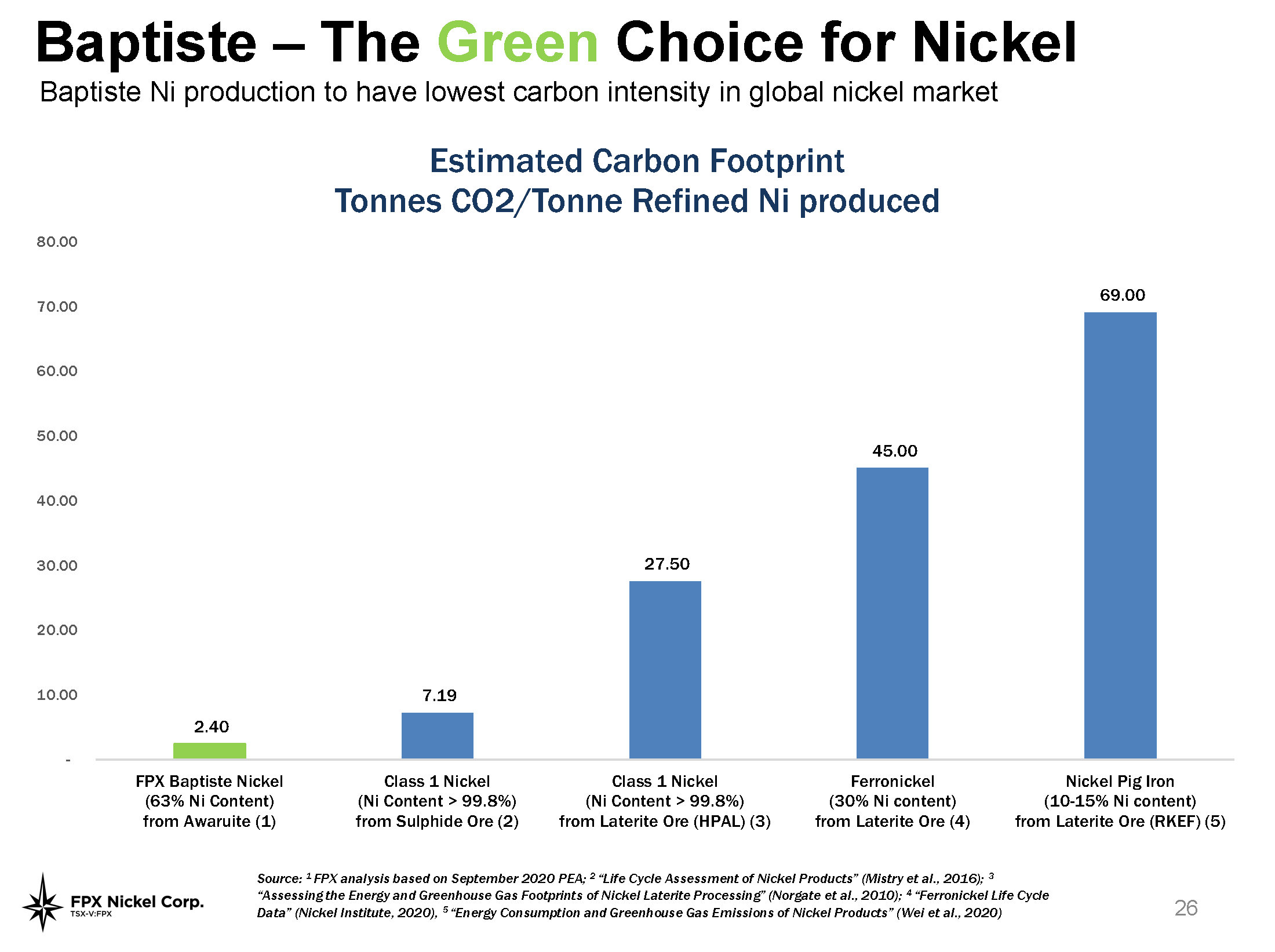

Martin: So we recently put out some disclosure that we’re quite proud of comparing the carbon intensity or the carbon footprint of our proposed nickel operation versus other different types of nickel supply globally. So the mining business by its very nature one that is carbon-emitting. You have typically diesel-fueled mining trucks running around, and then you’ve got a milling plant that oftentimes can be fired by coal or powered by coal-fired power plants. And so the emissions associated with the nickel production globally tend to be quite high sometimes. And in fact, you can run into a circumstance where a lot of the nickel that goes into these batteries right now could be characterized as sort of dirty nickel and nickel that in a way kind of obviates the case for even wanting to buy an EV, because if you want to buy an EV to lower your carbon footprint, but the source of the metals in that battery are ultimately quite dirty, the net benefits to the environment is potentially negligible.

The advantage that we’ve shown with our project here is given the efficient operating parameters around mining and processing, the fact that we’re on the hydroelectric power grid here in British Columbia shows that we can produce nickel at a very, very low carbon intensity. And in fact, at really one third of the carbon intensity of the lowest comparable type of nickel production out there. So, we think going forward where your position on the cost curve is always going to be fundamental, with mining projects, you want to be low on the cost curve, but we also think where you’re positioned on the carbon curve is going to start to become more and more important.

This ties into some regulatory push that we’re seeing in places like Europe, where they’re going to be imposing limitations on the carbon footprint associated with EV battery production. So if you going forward, if you want to sell an EV battery into the EU market, as an example, it’ll have to have a carbon intensity below some certain threshold. And so dirty nickel will really not be able to find its way into that product, which puts a bit of an advantage on projects like ours that can produce nickel in such a clean way.

Bill: What would you say to an investor that just sees your company as a leverage play on nickel? Do you consider that to be an accurate statement?

Martin: I think like any junior mining company, we are by our nature leveraged to commodity prices typically. And so I think that’s true of any junior company, particularly those that have defined resources. But I don’t view FPX as a leverage play on nickel in the sense that I think you’re alluding to. For us, it comes back to the fact that the world needs to be able to build new nickel mines. And so what are those deposits that can be built in the next generation of nickel mines? And what is the profile, the economic profile of those? And I think what our study shows is that we are at the top of the list in terms of capital intensity. So dollars of capital for every unit of nickel that you can produce and importantly, very low on the cost curve. So we’re not sort of an optionality play that requires a higher nickel price. In fact, at $2.75 a pound production costs, we’d be profitable if the nickel price declined by an excess of 50% from its current level. And so for us, it’s less about being an optionality or a leverage play on nickel and far more about having a project and developing it and showing that it’s really the leading project in the peer group.

Bill: So if an investor pointed out the CAPEX required, which is quite high, over a billion dollars, what would your response be again, to those that are looking at it only as a leverage play?

Martin: So first of all, it is the very nature of large-scale nickel mines such as what we have envisioned here, that they’re heavily capital intensive. So if you look back at the last boom in terms of the nickel mine construction, which was in the 2010 to 2012 period, you’ll see that the mines that were built by the major companies like Glencore, Vale, BHP, they had an average capital cost of around $4 billion. And so the nickel business in some ways is like the large-scale porphyry copper business. These tend to be multi-billion dollar, multi-generational projects. And so, as strange as it may sound, a CAPEX in the $1 billion to $2 billion range for a project of this scale and this mine life is actually a lot lower than what was expended by those major companies in the last cycle.

And so, does that mean that a junior company like ours necessarily has a clear path to building this project ourselves? No, not necessarily, but what it does demonstrate is that when the major companies of the world, or when capital providers are ready to start providing capital for the next leg of nickel mine construction, they’re going to look out and say, “Well, where can we build the most amount of nickel unit production for the lowest capital?” And on that scale, FPX actually ranks very well.

Bill: Martin, when I was reviewing your corporate presentation, as you mentioned, a clear rerate in the share price would be due to just getting at an equal level to your peers, but another catalyst potentially is your Van target at the Decar project. Talk to us about this Van target.

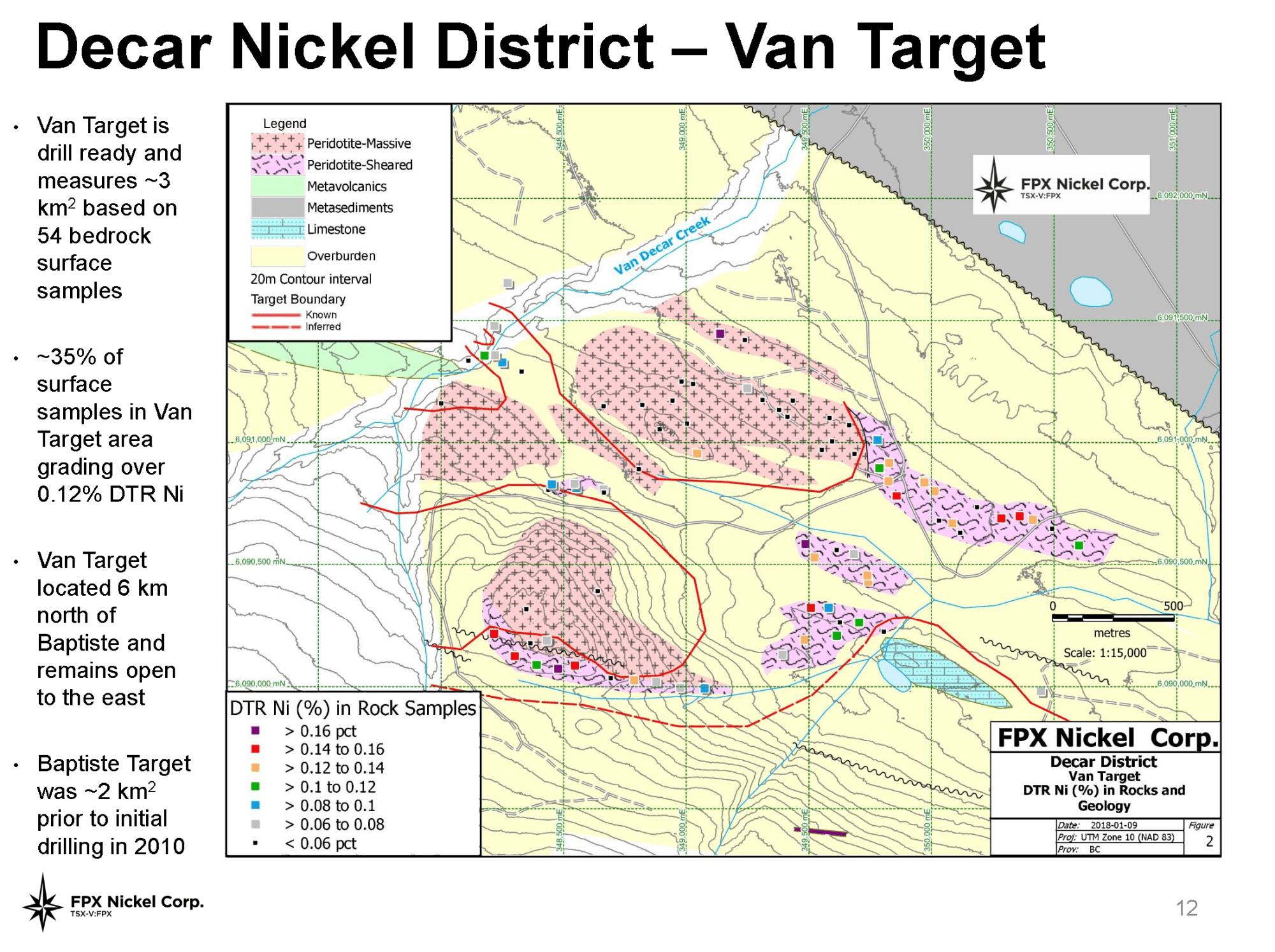

Martin: The Decar land package is large. We do think of it as a district. It covers 245 square kilometers. So within that, the Baptiste deposit, which supports the PEA and it’s one of the largest nickel deposits in the world represents only about 1% of that land mass. So there’s massive exploration potential that we’ve identified in geological reconnaissance work throughout the rest of the project that suggests there could be multiple deposits of that scale within the land package. Most notably at the Van target, where we have delineated a drill target there based on outcropping surface samples of bedrock that covers an area about three square kilometers of outcrop. So that is the target scale. By way of comparison, the lateral footprint of Baptiste is only about two and a half square kilometers. And the other thing that we see at Van is not only is it larger in its scale conceptually at surface than Baptiste, but the grades are higher. The grades are about 10% to 15% higher in surface samples.

Van has never been drilled. It had been previously inaccessible to us due to dense forest in the area, which has been cut away by the logging companies that are active in our area. So that’s allowed us to go in to take those samples and to initiate this summer, the first ever drill program at Van with a potential to delineate or to demonstrate that we have another world-class ore body within the land package. And I think that’s something that investors, oftentimes I find when I talk to them, they aren’t even aware that we have that. And it certainly, we think not at all reflected in our share price.

Bill: Copper drill stories, the successful ones, are getting a lot of attention and increased market cap, same thing with the precious metals. How have nickel discoveries been doing in the last 12 months?

Martin: Nickel discoveries always do well because of their rarity. The market loves nickel discoveries, and we’ve seen other companies come to market over the last 12 to 18 months. Drill off discoveries, whether they’re high grade underground style targets in Australia or big bulk tonnage scale discoveries in Canada, similar to what we have at FPX. And so we know the market loves discovery, and that’s certainly what we see with this Van target, this year has a potential to have a major nickel discovery within the land package.

Bill: And how many meters will you be drilling?

Martin: We have an initial plan for about 3,000 meters of drilling, which doesn’t sound like a lot. However, this style of mineralization is disseminated and very homogeneously distributed, which means that you can do very wide-spaced drilling and prove up tonnage very quickly. Just to give you a sense, we’ve done about 32,000 meters of drilling at Baptiste and proved up a resource that’s about two and a half billion tonnes. So the amount of tonnage per meter drilled there, that ratio is very, very high. And it’s due to that sort of very homogeneous distribution of this style of nickel mineralization that we have, which means a couple things. One, we can be very efficient with our dollars and prove up tons very quickly. And the other thing about this style of mineralization is that the visual returns that you get as you’re pulling core up, tell you a lot. And so it gives you great flexibility from a drilling standpoint to expand programs or to move the drill around as need be without having to wait sort of that two to three month period for assays to understand what you in fact have.

Bill: One of the things I liked about your share structure is that if you do hit a discovery and you get more market attention, your share structure is actually poised to where there’s not going to be that overhang of warrants that often limits junior mining stocks. Talk to us about your share structure, please.

Martin: Yeah, that’s an important point. So we have just over 180 million shares outstanding. The company has been public since 1996 on the Canadian, on the TSX Venture. So for a company that’s almost 25 years old to have less than 200 million shares outstanding is good. And I would note importantly, we’ve never done a consolidation or a rollback of shares. So I think it speaks to our discipline around dilution over time. The nickel market and the junior market as you well know, Bill was struggled mightily from the 2014 to sort of 2019 period. And over that span of time, as we did financings to advance the project despite the very difficult conditions, we never issued a warrant during that period of time. And so there are no warrants outstanding on the stock. And that just speaks to our, again, discipline around dilution, wanting to preserve that capital structure and not have any kind of artificial ceilings on the share price.

The other thing I would note is the very high level of insider ownership. Insiders or management and board own over 21% of the company. And again, for a company that’s been around for 25 years, that is pretty remarkable. I’m not aware of other companies who’ve been around for nearly that long having that degree of insider ownership. And that just speaks fundamentally to our belief in the project and our alignment with day-to-day retail or institutional shareholders.

Bill: And how did you acquire your shares, Martin?

Martin: All my shares has been bought either via a private placement or in the market. So there’s no founder’s shares. Twenty-five years ago FPX Nickel wasn’t on my radar.

Bill: Treasury and burn rate. What are we looking at here?

Martin: Yeah. Okay. So current treasury sits at about 5.9 million Canadian and our budget expenditures, including drilling, metallurgical programs and other work programs this year and G&A is about $3.8 million. One of the things that we’ve always prided ourselves is a very low G&A burn rate. So in previous years, our G&A burn rate has been in the region of around $500,000 per year. That covers all salaries, rent, marketing, et cetera. And so it’s something we study quite closely and we see that for companies in our peer group, that’s about one quarter of what companies typically spend on G&A. So we’re actually quite proud of that. And again, just shows the focus on discipline.

Bill: And you’re also an accountant. I think we should point out on that note, right?

Martin: That’s right. Yeah. The bean counter tends to be tight with the pens, for sure.

Bill: You have been thrifty. I was going to say that in the introduction I would call you thrifty. And I meant that as a compliment, not as an insult, of course, as you’ve demonstrated with your share structure over that many years. Let’s conclude with catalysts for 2021. Succinctly summarize for us, what are the upcoming catalysts?

Martin: There’s three main areas we’d like to focus people on for this year. The first is the continued work that we do to demonstrate that this can be a very low carbon operation. So we’ve shown in a recent news release that we can have a very low carbon footprint and very much lower than our competitors in other types of nickel production. We also have the ability at this project to actually sequester carbon dioxide in our tailings and something we can perhaps get into at a later time. But we think that ultimately our tailings can act as a natural carbon sink and make this potentially an operation that has a net zero carbon footprint. And so there’ll be more news on the research and the testing that we’re doing to demonstrate that. The second piece would be metallurgical testwork. So very strong metallurgical testwork went into the PEA.

We’re now embarking on metallurgical testwork that would serve to support an ultimate pre-feasibility study on the project to validate the findings in the PEA, and potentially to see if we can have improvements in recovery. One of the important elements of that as an output will be for the first time we’ll be using our concentrate to produce nickel and cobalt sulfate. We do have cobalt in our product as well. And nickel and cobalt sulfate are the key battery chemicals that go into production of EV batteries. And so for the first time ever, we anticipate being able to produce those products according to the very exacting specifications that are required by the battery makers. So that’ll be an important catalyst for us, an important milestone as we go forward this year. And then the third piece, I think is just as we talked about that Van target drilling. We see the opportunity here to delineate a mineral deposit that may be richer in grade or potentially larger than Baptiste or potentially both.

And so, our current valuation is underpinned entirely by Baptiste. And if we can demonstrate that we have another very large-scale world class nickel ore body at the project, we think as we said, markets love discovery, and that would inherently add a tremendous amount of value to our story.

from Kerry Lutz Podcasts – Financial Survival Network https://ift.tt/3rffK37