Top Finance And Economic News Today. Your one stop site for news about USA and global economy, gold, silver, investing, geo politics, mining stocks.

We cover news about and from Jim Rogers, Jim (James) Rickards, Mike Maloney, Peter Schiff, Greg Mannarino, Greg Hunter, SGT Report, Robert Kiyosaki, Martin Armstrong, Bo Polny, Eric King, King World News, Bix Weir, Paul Craig Roberts, Dollar Vigilante and many more.

Today multi-billionaire Hugo Salinas communicated to King World News that gold is back! as the BIS just caved under enormous pressure from Russia and China.

We’ve known James Corbett since we started in media. He’s a forward thinker and all of his statements and opinions are always backed up with facts. We’re a big fan of his work. You’ll be shocked by the things he discusses in this interview. There’s a certain segment of the ruling class that are planning for humanity to be superseded by a new species that will be a combination of humans and AI based technology. Scary but very fascinating.

Today the man who has become legendary for his predictions on QE and historic moves in currencies and metals told King World News that people need to get out of the financial system now!

CEO Stephen Stewart still believes Orefinders (TSXV:ORX – OTC:ORFDF) could one day deliver “that billion-dollar drill hole.” In fact, that is why he negotiated a deal with Kirkland Lake Gold where they can earn up to 75% of Orefinders’ Mirado, McGarry and Knight projects in exchange for spending C$60M on these projects. Stephen believes this deal eliminates the dilution and financing risk for Orefinders’ shareholders while simultaneously increases the possibility of producing “that billion-dollar drill hole.”

Orefinders is gold explorer with the third largest land package on the Ontario side of the prolific Cadillac break in Canada and is about to commence six to nine months of non-stop drilling at its projects. In addition to the tremendous discovery potential, the company has an approximately one million gold ounce resource (historic and NI43-101) at its three projects combined as well as three control block positions in three prospective junior miners. In this interview, CEO Stephen Stewart explains why the deal with Kirkland Lake Gold makes sense for Orefinders’ shareholders and how it better positions the company for a potential major gold discovery.

Sign up (on the right side) for the free weekly newsletter.

0:00 Introduction 1:17 Why ORX deal with KL makes sense 6:16 We’re designing our future drill programs with KL 9:38 ORX pace moving forwards? 10:51 How deal benefits both MIS & ORX shareholders 12:07 Increased odds of “billion-dollar drill hole” 12:54 Huge inefficiency in how MIS & ORX are currently priced 14:23 Trading at only $10-12/AuOz in the ground 15:41 Possible risks 16:46 Next 12mos

TRANSCRIPT:

Bill: Thank you for tuning into Mining Stock Education. I’m your host Bill Powers. Joining me today is Stephen Stewart, the CEO of Orefinders, One of our sponsors. I invested in Orefinders back when we originally previewed them and profiled them last fall. The share price I got in at was about $.10 Canadian. After that, it went up to about $.25 Canadian. At one point, I was 150% up. Right now, I’m under water. Actually, it’s been trading as low as $.07 cents in the last week, so I invited Stephen back onto the show. Stephen, tell us what’s going on. You did this deal with Kirkland Lake Gold. The market seems to have not valued it and seen it the way that you’ve seen it. I’m underwater on my investment right now, convince me to keep holding your company please.

Stephen: Well, sure. Thank you for having me Bill. First and foremost, I think this deal is a great deal for shareholders. And of course, it did the same thing with Mistango as well. I think it’s important to say this was a joint deal between the Mistango and Orefinders, so both companies did nearly an identical deal with Kirkland Lake. Why I think you should continue to hold your shares is because this completely de-risked the company. Now, there’s always going to be risk in this business, but it’s a very, very risky industry that we’re in. I’ve been on your show and I’ve said many times before, we are after a billion dollar drill hole, both Orefinders in Mistango. We are in the right district. We have the right rocks. We think we have the right team. And now, we have a lot of capital to go out and do it.

When we approached Kirkland Lake to do this deal, it was really fundamentally about increasing our odds of achieving success. Success comes in many ways, but if we are going to do… achieve a billion dollar drill hole, which is a new discovery on that trend, it’s going to take more than one or two or 10 drill holes. That is what this deal ultimately represents to shareholders. It’s mitigating our downside risk. If we do not want to live or die on our last most recent drill results, which is what a lot of juniors do. This was me and our board building a future, building a company. That’s what that represents.

Now, for those who don’t know, the deal Kirkland Lake came in and acquired 9.9% of both companies, so they own the shares and then they are spending up to $120 million split equally between Orefinders and Mistango to earn up to 75% interest in those company’s assets. That means $120 million will go into the ground before Kirkland Lake earns their interest. In effect, that gives us a free carry until they spend that money and that’s an awful lot of money. I would wager that if we spend $120 million and we don’t find a billion dollar drill hole, then it’s not there. I think this allows us to exhaust all the possibilities and probabilities that if there’s an orebody there, chances are we’re going to find it.

In the meantime, we’ve got this fantastic treasury between Orefinders and Mistango, approximately $15 million in cash. Over and above that, we have well over $20 million in working capital, which constitutes mostly Orefinders’ position in equitable securities. It owns a good chunk of Mistango. It owns a good chunk of QC Copper and same with American Eagle, which has spun off. We have an extraordinarily strong balance sheet. Those who follow our group will know we’ve had a very contrarian view of the market. The last five years has been spent with Orefinders and subsequently Mistango identifying opportunities, buying them cheap when nobody else was doing and looking for distressed situations, looking for problems that we believe we can buy cheap and then solve and create value there. That is going to be… Really, my task right now is intelligently allocating that $15 million. Where are we going to spend it to get the best bang for our buck? At the same time, we’ve got Kirkland Lake Gold funding us in our operations to go after that billion dollar drill hole.

I thought this was a deal that we couldn’t pass up. I think honestly, it’s enviable. I think there are… I don’t want to speak on behalf of the entire junior industry, but I absolutely know that my contemporaries and competitors would absolutely love to have a group like Kirkland Lake Gold in their corner. I think it just opened a lot of doors. It brought visibility. Retail investors can rest easy. When you get a big company, best in class, like Kirkland Lake, willing to invest in the team and the assets, that alone says something about the team and the assets. They don’t put their money anywhere. They are very choosy because they can be and they invested in us and that’s just a level of due diligence that I think your typical retail investor can sleep a little bit better. That’s how I feel about it.

The last point I make, I’m buying the shares, Bill, so I’m putting my money where my mouth is. I’m in the market. I’m buying. On Orefinders, just for the record, I am not able, as a securities law issue, I’m not able to buy Mistango shares in the market because my personal position. I’m the third or fourth largest personal shareholder of Mistango, but securities laws lumps me together with Orefinders, so our position together over exceeds 19.9%. Hence, I would trigger a takeover bid if I did buy Mistango shares. I participate through through Orefinders, which has a position in Mistango anyways.

Bill: So Stephen, there’s a lot of people that I talked to, including Rick Rule, who I just interviewed this week, they really like the Prospect Generator Model. They acknowledge though that it requires patience in a longer term outlook. Myself and a lot of people listening to us are more impatient. I’m impatient. I’m just telling you I’m impatient as a speculator. I’m being very aggressive. I’ve invested in your exploration companies, other exploration companies. It’s too large of a percentage of my portfolio. For most people, I would never advise doing what I do in terms of percentage and exploration companies because I’m very aggressive in what I believe to be a gold up cycle. When you get an impatient investor invested in your company, looking at Orefinders last year, I thought we would get drill results over the next 12 to 18 months and I’m looking at a five plus… 10 bagger. Now, yes, you’ve minimized the downside clearly. The dilution risk is gone, the financing risk is gone, but you’ve also given away 75% of the upside. I’m also wondering what is my timeframe now because I’m impatient. Is it still 18 months? Can I get a five bagger? Or is it more like five to seven years? What are we looking at here?

Look, things can change on a dime in this industry. Speaking of drill results, both companies have finished drilling this particular campaign, but Mistango’s got 33% of its asset is outstanding from this program, this highly anticipate. We’ve only released 66%. We didn’t hit it yet, Bill, but we got 33% of those holes to go. Then last week, we were up in Kirkland Lake, sitting down with Kirkland Lake Gold, designing our future drill programs. Same thing with Orefinders and Orefinders also has 17% of its assets outstanding. So both companies, things could change very quickly tomorrow off past drill programs. We’re absolutely going to be drilling tomorrow, so nothing changes. Things can change very quickly in this industry. Just wait to see what happens if us or anybody hits a big drill hole next to a major mine.

As you know, Mistango is focused primarily on it’s Kirkland West Project, drilling beside Macassa. The stock, I think, would go through the roof if we could delineate a nice intersection right beside Macassa. That prospect, nothing’s changed. In fact, we’re better capitalized to do that. Now, Orefinders, the same thing. It’s next drill program is going to be on, it’s McGarry. It’s really quite analogous to Macassa and our Kirkland West Project. McGarry is located directly adjacent to the Kerr Addison. For people who may not know, the Kerr Addison was the Macassa of its day. It produced for 50 years, over 11 million ounces of gold, the high grade. It’s just like Macassa and it’s 20 kilometers to the east. We have the property next door. Orefinders just completed an IP and an MT, magnetotellurics survey, to look deep because that’s where we believe we’re going to find an orebody if it exists on the McGarry and that’s where we’re going to be drilling soon.

If we can poke a hole into McGarry and do the same thing we’re trying to do on Kirkland West beside Macassa, well, look, things would change awfully quick, Bill, especially as gold is approaching $1,900. We’re back out there exploring. Nothing has changed and things can change quickly.

Bill: I agree with you that the amount of money you were able to get Kirkland Lake to potentially commit is impressive, but my main concern, honestly, was the pace. What pace are we going to move? Because you need them more than they need you. Are you telling me that the pace is going to be at least what you were planning to do before this deal? Is that what I’m hearing?

Stephen: Well, I don’t think… I can’t speak to the pace that it’s going to go. We’re going to go one step at a time. We are absolutely going forward with a drill program on Kirkland West. We’re going back out there. The same thing for McGarry. So first things first. I mean, as far as pace goes, expect us in the, not too distant future… I don’t want to say time because we’re just sitting down with Kirkland Lake and talking about the program, but largely they are looking to us. Nobody knows our projects better than us. They are asking our opinion, but we’re certainly soliciting theirs as well, particularly on the Kirkland West where they know exactly where to drill. That’s going to be very valuable information. So in terms of the pace, I think investors can expect us, in the not too distant future, to come out there with the second iteration of their drill programs for those properties that I’m talking about. We’re pushing as quickly as possible. We’re permitted. We’re ready to go. Let’s do this

Bill: Stephen, one of the things that was articulated online was that the Mistango shareholders didn’t want to be grouped together with the Orefinders’ shareholders. Can you talk to that situation because you’re a leader of both? Perhaps did you treat one child a little better than the other in arranging this?

Stephen: Well, absolutely not. Literally, both companies were virtually identical in terms of their cash position and their market cap. They have different assets and different possibilities, but ultimately at the end of the day until you find a discovery, you can’t say one has a better shot or not. Both have assets that are adjacent to world-class mines. As I said, the Kerr Addison for one and Macassa the other, and they have secondary assets as well, with both very substantial 43-101 resources. It’s a matter of opinion and my opinion is that the companies were treated exactly equally. The deals were identical, in terms… Kirkland Lake invested 9.9% in both. The earn-in options for $60 million each, so $120, were identical. I can’t imagine how any company was treated any differently. In fact, they were treated equally, were like twins.

Bill: So you haven’t given up that billion dollar drill hole because that’s something you mentioned the first time. You just feel like you haven’t-

Stephen: Giving it up, I’m after it and this increases our odds. We don’t want to live or die on our last drill result. That is a very difficult business model, especially in the junior mining industry. We have covered our downside, that if any one of these projects do not deliver that… And Bill, let me tell you, odds are you do not get that billion dollar drill hole. I mean, HELMA was found on hole 84 and there are many, many other examples. Could you get lucky? Of course, you could. Do I want to get lucky? Do I want to come out with a billion dollar drill up tomorrow? Of course, I do. But odds are, we’re not, Bill, and hence why we did this smart deal with the best partner in town.

Bill: So Benjamin Graham, he said, “In the short term, the market is a voting machine. But in the longterm, it’s a weighing machine.” Do you think that applies to what we’re talking about here?

Stephen: Well, sure. I mean, there is no more inefficient segment of the publicly traded stock market than the junior mining industry. It’s inefficient as it gets and it’s about identifying those inefficiencies to the upside and to the downside. And right now, I see a huge inefficiency in how Orefinders and Mistango are priced. Price versus value, as Mr. Graham always says and, of course, one of his proteges, Warren Buffett. The value baked into Orefinders and Mistango relative to the price you have to pay today is extraordinary. Look at their balance sheets, look at their investments in other companies and then look at the assets that they have combined with the partnership of Kirkland Lake, who is committed to spend $120 million, big, big numbers here.

Our enterprise value in those combined companies was $28 million. We signed a 75% deal at $120, not bad economics. I don’t see how anybody could blink an eye at that. I see huge value. And ultimately, everything comes down to our drill results, which could change any day. So as long as we’re drilling, which is going to be the secret to our success, then I sleep well at night in terms of delivering what I said I would do to our shareholders.

Bill: All right. So with speculative value through the drill hole, we’ve been talking about that, but you also have resources. Just if we take enterprise value versus gold ounce in the ground, what are we trading at right now?

Stephen: Enterprise value right now, let’s say we’re $14 million… $10 to $12 an ounce, nothing really. We are not in the Arctic. We are not in the DRC. We are in Kirkland Lake Gold, excuse me, Kirkland Lake Ontario, no better place to be on the Cadillac, which is extremely prolific. And I’ll note, in an area where there’s an awful lot of activity. Not only do we have Kirkland Lake and their flagship operation, we’ve got Agnico Eagle with the Upper Beaver there. We’ve got the Kerr Addison. I mentioned the Kerr Addison, a world famous mine. They have now reinvented themselves as a six million ounce open-pit deposit. They floated their perspectives not too long ago. We’ve been aware of what they’re doing. That’s coming into the public domain, so we’re thrilled to welcome new neighbor, a major, major anchor type deposit.

There’s all sorts of things happening. I think even the folks that New Found Gold are spinning off their property in the Kirkland Lake. There’s an awful lot of activity up there. All else equal, there’s no other place I’d rather be looking for gold right now, other than Kirkland Lake.

Bill: With an explorer, the obvious risk, key risk, would be coming up with dusters an, not discovering what you want to discover. But besides that, over the next 12 months, what would be some of the key risks for Orefinders?

Stephen: Oil price. The toughest challenge we have is mother nature. There’s no question about it. That’s the risk people take and it requires patience, but I understand that investors are impatient and they see things, fast money, and they chase it. I get it, but that’s not how to run a business. You have to look over the horizon for the longterm, cover your risk, but keep the upside. And boy, do we have upside. So outside of us working our projects, don’t forget, we’ve got this $15 million to deploy and we’ve been pretty creative. Anybody that’ll look us up, we have been creative in how we deploy our capital. We do it quite creatively. We took over Mistango River Resources for $250,000. That was in a different market, but that’s the sort of deals that we like to do and that’s… So with $15 million to deploy, we’ll see what happens.

Bill: Okay. As we conclude, the final question for this impatient mining speculator, 12 month target, you got to put a carrot out in front of this rabbit. What should I expect? What’s the goal, 12 month target? Give me something to visualize here.

Stephen: Share price. Oh God, I never prognosticate a share price. There’s just too many variables. I don’t think that’s the right thing to do, except that I think we’re going in the right direction. I think right now… Let’s talk about where I think the low is. I think right now, we’re not going to get any cheaper. That I can feel very comfortable saying. Whether we’re going to be $.50 or $1. mother nature, plus gold price, those are the variables that will have the biggest say in where we’re at. But I think in terms of, if you want a quality team that’s well financed with assets and excellent jurisdictions, world-class jurisdictions, next to great world-class mines with the backing of Kirkland Lake Gold, take a look at Orefinders, take a look at Mistango.

from Kerry Lutz Podcasts – Financial Survival Network https://ift.tt/3oYmLp4

Fury Gold Mines (Ticker on TSX/NYSE: FURY) just released significant drill results. It drilled a top five intercept to date – 23.27 g/t gold over 7.09 meters outside the defined resource at Eau Claire. The last time we spoke with CEO Mike Timmins, he assured us the pace of results was quickening, and clearly he has over-delivered. He and Michael Henrichsen (Exploration SVP) came on to discuss the impact of the latest news.

Results have been coming in at a rapid rate. It was just a week ago when the company announced it found more high-grade gold in the adjoining Snake Lake structure. In addition it identified a new mineralized horizon between the Eau Claire and Snake Lake structures.

Timmins expressed the belief that Snake Lake could have the same size potential as Eau Claire, which would greatly increase the scale of the project. He commented, “This is the kind of project that everyone is looking for… We’re just getting started, 7 months in.”

As noted mining analyst and newsletter writer David Erfle recently observed, “[The] Junior Gold Stock Fire sale is probably over…” And as the market recognizes the great potential of Fury, the recent rise in its share price is further evidence in support of that view. If things continue on the way they have, there could be a big payday ahead for Fury’s shareholders.

By all appearances the Covid-19 pandemic appears to be winding down. After the great disruptions and chaos of the past year, people are now wondering how to resume their normal lives. Many of you are suffering from PTSD. Some people just can stand the idea of giving up their masks in public. Then there’s the issue of re-starting your social life. And what about those who have4 suffered grave economic injury, how do you put it all in the past and move? Noted clinical psychologist Dr. John Huber gives some solid easy steps you can take to create a new normal that’s even better than the old one.

When we last spoke with Torq Resource’s (Tickers: OTCQX: TRBMF – TSX.V: TORQ) Executive Chairman Shawn Wallace (sponsor), he hinted that another major acquisition was on the way; in little more than a month, he’s delivered. Torq has optioned the Andrea Copper Porphyry Project, providing the company with an excellent opportunity to discover a world-class copper porphyry system. Its on the ground geologist network has done it again. Wallace indicates that further acquisitions should be expected. At the rate he’s been going, Torq has a great future prospects. With the recent surge in copper prices, the company is uniquely situated to build a portfolio of top-tier copper projects.

For more than 20 years, Master Trader Nick Santiago has been beating the markets. He’s made some incredible calls along the way and now he’s looking to spread the word. There’s no reason that the average trader should be coming up short. So now we’ve started a daily show to bring you up to date on the latest market developments. Nick will be sharing trades and concepts and discussing current trends.

The Fed is telling you that the current bout of inflation is just a temporary phenomena. But is it? Noted financial advisor Gil Baumgarten thinks otherwise, it could very well be here to stay. We discuss what will happen to bonds, stocks and real estate in this new economic environment. And don’t forget about gold and silver either.

For more than 20 years, Master Trader Nick Santiago has been beating the markets. He’s made some incredible calls along the way and now he’s looking to spread the word. There’s no reason that the average trader should be coming up short. So now we’ve started a daily show to bring you up to date on the latest market developments. Nick will be sharing trades and concepts and discussing current trends.

According to Dr. Dean Fanelli, PHD, the vaccine implementation has been a great achievement. It’s time to look back and get a better understanding of where the government, the CDC and Dr. Fauci went wrong. We’ve received conflicting signals about lock-downs, masks and social distancing. The CDC went from all masks all the time to no more masks necessary. Perhaps now they’ve gotten it right. School closings were also way off the mark. We also talked about the admin’s desire to give away the vaccine IP to all takers. Probably not a good idea. There’s a complex web of patents and the ability to manufacture the vaccines make such a giveaway difficult and not effective.

Craig Hemke gives us the real story on transitory inflation. No one is focusing on why they’re saying it. It’s all about yield curve control. The US cannot afford higher interest rates. The Fed is controlling yields and real interest rates. Interest on treasury debt cannot exceed 2 percent or we’re all scr-wed. It’s a case of Fed jawboning to shape perception and reality. After this fails, they’ll have go to policy pronouncements. And when that fails, then they will actually have to do something. The biggest question is, who will buy US government debt when it’s yielding less then inflation? Answer: the Fed. Repo madness strikes again. Reverse repos are hitting record levels, spiking. Banks are over-stuffed with reserves. Lots of interesting stuff going on, setting us up for an interesting month of June. 3 weeks to the next FOMC meeting. Fed said they’re going to lengthen the maturity curve of their QE program. Shorter term maturities have been crowding out buyers and driving short term rates to near zero. So the Fed is on to 5-7-10 year debt. This is what yield curve control is all about. Gold continues to progress higher off the double bottom. In case you hadn’t notices, we’re currently in a gold bull market. $2300 gold is right around the corner. Get ready. On the inflation front, we’re seeing cost-push and demand pull inflation. Higher wages are being used to entice workers back into the labor force. Negative real rates equal higher gold prices and we ain’t seen nothing yet.

Sign up (on the right side) for the free weekly newsletter.

from Kerry Lutz Podcasts – Financial Survival Network https://ift.tt/3fjFIPN

What’s the secret to driving demand, and generating leads and revenue online? What’s a digital transformation, and why do some companies succeed while others fail? And how do you stage a winning digital pivot? In his book, Eric Schwartzman explains what successful digital marketers do differently. This is the inside track on how to pivot to digital marketing in four easy steps, so you can earn more and work less.We are living through a time of unprecedented migration, from analog to digital business practices. Find out what it takes to stake your own claim online, so you can participate in the ever-growing digital economy, and get your share of the profits. Through real world stories and numerous examples of digital marketing pivots told in easy-to-follow, nontechnical language, you’ll learn the secrets of what it really takes to be competitive online, so you can increase revenue, decrease costs, and control your future.

For more than 20 years, Master Trader Nick Santiago has been beating the markets. He’s made some incredible calls along the way and now he’s looking to spread the word. There’s no reason that the average trader should be coming up short. So now we’ve started a daily show to bring you up to date on the latest market developments. Nick will be sharing trades and concepts and discussing current trends.

Andy Schectman notes that the Perth Mint’s unallocated, pooled account program appears to be in trouble. People seeking delivery or allocated metals have been complaining about major delays or even a failure to delivery. In their recent annual report, they indirectly admit that they don’t have the metal. It’s been re-hypothocated to the moon. Advice, especially now, never, ever buy unallocated anything. Andy says that Perth has been a great supplier of physical silver to his company. Beware of counter-party risk. It’s evidenced by the recent run on Comex. Beware of SLV and GLD. Inflation and interest rates have been heading higher and have no where to go but up. Money printing is completely out of control. Inflation is running 3-4 times higher than the nominal interest rate being paid on treasuries. It’s a very precarious position. They can’t raise rates to attack inflation. Until you see rates rise above the rate of inflation, there’s plenty of room to go higher in the gold and silver market. Basel 3 June 28 of this year the new net stabilization rules go into effect. The mandate will increase 85 percent collateral in metlas markets, up from nearly zero now. More on that later.

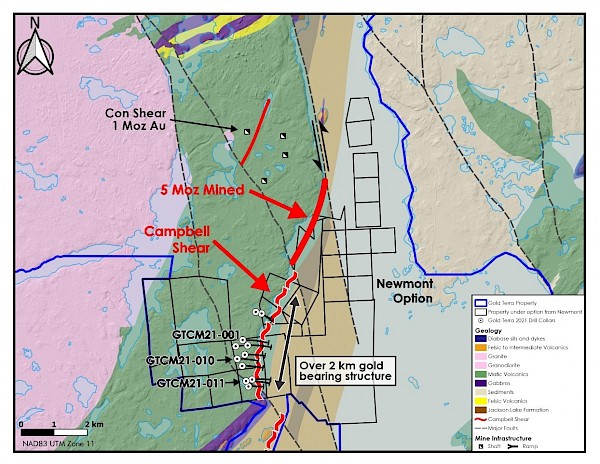

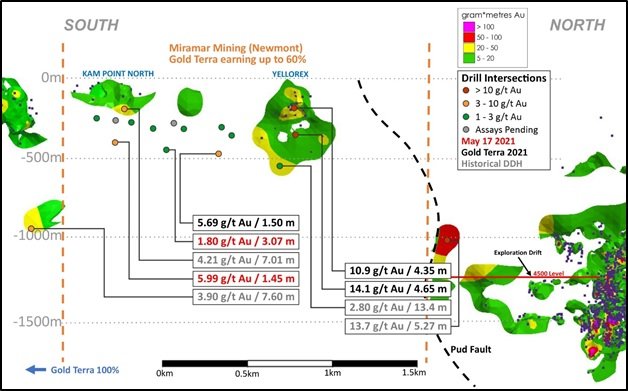

Executive Chairman Gerald Panneton discusses Gold Terra’s (TSXV: YGT – OTC: YGTFF – FSE:TX0) completed phase 1 drill program at its project immediately adjacent to the high-grade former-producing Con Mine (5+M AuOz) outside of the city of Yellowknife in Canada’s Northwest Territories. Gold Terra recently acquired an option on this property from its owner Newmont. The Con Mine produced approximately 5.1 million ounces of gold between 1946 and 2005 at an amazing grade of 15 g/t, and over widths of up to 100 metres. Gerald said that this phase 1 program confirmed the extension and continuation of the Con Mine’s mineralization onto Gold Terra’s optioned property and was thus successful. Phase 2 drilling of 10,000 metres will begin in July and will produce drill result news flow consistently from August into the fall.

Sign up (on the right side) for the free weekly newsletter.

0:00 Introduction

0:35 Phase 1 10,000m drill program completed

3:45 Was phase 1 successful?

4:53 Covid a hindrance at all?

6:47 Cost of drilling

8:25 Results of phase 2 Aug-Nov

9:05 30,000 to 40,000m winter drilling

9:37 Gold sector M&A

13:10 Bitcoin or gold?

TRANSCRIPT:

Bill Powers: Thank you for tuning into Mining Stock Education, I’m your host Bill Powers and joining me today is executive chairman Gerald, Panneton of Gold Terra Resources Corp, one of our sponsors. Ticker symbol is YGT in Toronto and YGTFF in the States. Gerald, welcome back onto the program. We’ve been talking about how you are engaged and have just completed phase one of a drilling program South of the Con Mine outside the city of Yellowknife. Now the Con Mine, for listeners that aren’t aware, produced about five to six million ounces, historically, of high grade gold and Gerald optioned this project from Newmont and believes that they can discover the extension of the Con Mine. So a 10,000 meter program. Phase one was just completed. Please walk us through this program Gerald. What are the results and what is the significance that investors should know at this point?

Gerald Panneton: Thank you very much, Bill, for inviting me on. We’re very happy with the first program. The first phase was basically… There’s been no drilling for the last 30 years along the strike line of the Campbell Shear. And as you mentioned, Campbell Shear five million ounces, an average grade of 15 grams, or a predecessor of Newmont on the Con Mine, which shut down in 2002-03, approximately. And when gold price was very depressed. And there’s still a good resource on the Con Mine, the project now is under liability, but the Campbell Shear is a structure that is 70 kilometers strike length. And immediately to the South, there’s been some resource outlying. And as you can see on the long section and on the mapping that shows… The surface map, which shows the drill hole location we did, we did 13 holes this past winter, and we’re going back in July.

So phase one was to outline the Campbell Shear, which is sometime 100 to 300 meters in width, and sometime has militarization. And sometime it doesn’t have some, but the moment you have, even with our last person leaves this week, like 1.3 grams per 10 meters in the Campbell Shear. You know you’re in the right place. It’s just that you need to drill more. For example, some of our first holes on Yellow Wrecks deposit in the coach meeting, which will be the target when we go back in July, mainly. We have 15 grams over five meters, 11 grams over four meters. That’s exactly what the Campbell Shear was all about. It’s four, five, six meters in width, goes to almost one gram over 10 meters, 100 on strike length. So these are pods they’re they’re lenses that pinch and swell and the integrity of the Campbell Shear there, it’s just if you’d need to drill more. And that’s exactly what we’re planning to do with phase two, another 10,000 meters and hopefully with a much bigger program next winter, but we’re at the right place. Campbell Shear is there, globalization is there and we just need to drill more.

Bill: From your geological vantage point, did you get the information that you were looking for in phase one to a plan out phase two?

Gerald: Definitely, the indication you can see it on the long section in the last press release or the one on Yellow Wrecks that we did about a month ago. Exactly. That we are… We know where the Campbell Shear is, we know its behavior, we know when the globalization is there. There are some ingredients such as the series that take alteration, the presence of gold. And when we have quartz veining, smoky quartz, usually we have higher, great mineralization and that’s it’s all about. And we’ve looked at all the level of plan of the Newmont Mine. We’ve compiled them. We’ve looked at the geology. In the mind itself, you go from one gram to 10 meters, you move 25 meters and you hit 15 grams over 10 meters or seven meters. This is exactly the same mineralization pattern or structural pattern… Behavior that was at the combine on the Campbell Shear is on the Newmont property South of the Con Mine that we are currently drilling.

Bill: So the plan I understand is to drill another 10,000 meters. With COVID… How is the COVID situation in Yellowknife? And could that pose a hindrance to what you want to accomplish?

Gerald: We have been extremely lucky. We started the program before the pandemic started. We were able to finish our program. At the end of April, we went back mid August, last summer, drilled pretty much all winter. Yellowknife is a city of about 25,000 people, 25, 30,000 people. And it lives a lot from tourists and from the mining… The diamond mining industry in the Northwest Territory as a platform to service them.

In reality, Yellowknife is pro-mining. It’s essential to do exploration. It’s essential to do mining because all the jobs depends on that. And basically we just follow the protocols. If most of our people are in town… Live in town, our technical team, except 1% that comes from the outside. And we run a very, very lean… Because before I joined their average cost was $275 Canadian per meter. And now we’re drilling for $200 per meters, all in. So we’ve really came down, becoming very lean about what we’re doing. And next phase program should be more exciting the first one. The first one we were trying to line up the Campbell Shear over almost two and a half kilometers of strike length. So we were drilling every 200 meters trying to position the Campbell Shear and its mobilization. Now we’re going to be focusing on more on Yellowrex, where we had the best result. And also closer on where we think that we should be able to identify a high-grade nemesis.

Bill: Gerald, so you haven’t seen your cost of drilling go up then? Because everything around me, housing, food, where I’m at, everything is going up, but your drilling contractor, isn’t sending you an inflated bill for phase two drilling?

Gerald: Well, as long as you don’t buy any wood, you’re fine.

Bill: Or soy beans or corn.

Gerald: That’s right. Well, the fuel is… It is what it is. So there may be a change in new fuel because a year ago we were at $40 a barrel, and now it’s $65 a barrel. So there’s always like a hit on the fuel. But at the end of the day now, we are using the same contract that when I started in November, 2019, and it’s the same contract with the same contractor. People respect a quarantine. Of course, it’s easy for people to work because you cannot just go. You’re being quarantined. You arrive in town. And if it’s a shift change for six week and you’re going to have the same driller for six week, then these two guys, they go to their room. In the first two weeks they have to have their food delivered to their apartment.

So everybody is respecting the protocol and we are able to work and we’re going back in early July. For the next phase of drilling and we look forward because this should be a lot more exciting than the past one. The past one was our first pass. We needed to make sure that we identify the Campbell Shear, we know where it is. Now, this time around holes will be shorter, tighter, and we’re going to ensure to have a lot more mineralized intercept.

Bill: So if you start drilling in early July, when should we start expect seeing results?

Gerald: Usually this hasn’t changed. We still are bound by six weeks from the moment, basically, we finish a hole, we log it, we send it to the lab. It’s a four to six week delay. So, we should start seeing resolved by the end of August.

Bill: And then all through October, maybe?

Gerald: August through Oct- September, October, November. 10,000 meters with one rig will take us approximately four months. And we’re not going to stop drilling from about July all the way to mid November. Then we’re going to take a break again, build our ice road, and hopefully with better funding in the fall, with good result, we look to maybe 30 to 40,000 meters of drilling next winter.

Bill: At the same Con Mine extension?

Gerald: Probably. It depends on our success, of course, it depends on how much money we can raise. But if you asked me “how about what you do next winter?” And I would say, if I raised the money for 40,000 meters of drilling, next winter, we’ll do it. We have some extension of the Sam Otto that we can do, but the main target will remain the Campbell Shear.

Bill: And Gerald, we’ve talked in the past that because of your experience at detour, you know how to build a mine, you have the flexibility to move the project forward into feasibility and beyond or sell it. In regards to selling, there’s been some M and A action, some all cash transactions. What is your current observation and commentary on what’s occurring in the Merger and Acquisition space within the mining sector?

Gerald: Well, everybody has an interest in growing their company. For us, growing the company is finding more ounces. My target on the Campbell Shear is 1 to 2 million ounces of high grade mineralization. It’s out of the Con Mine. And I think this is achievable. Now we have 1.2 million ounces at Sam Otto and Crestaurum. So you combine that together; 20 million ounces becomes really attractive because it’s size. It’s about size 10 years of production, 150,000 to 200,000 ounces a year. You know, this is something that becomes very valuable for any company. Building an underground mine is not like building Detour. I was the founder and CEO of Detour inception all the way through our first year of production in 2013 and building a big mine like Detour is… It’s a heavy lift, especially for a junior. Think about it, I raised $2.6 billion over the course of my time at Detour.

And $1.5 billion or 60% of that money went into building the mine alone. And I still remember having to raise money in 2015 when gold price went down from 17 to 1100. Now we have a great timing goal is approaching $1,900. Again, we know very well, and we can talk a little bit about what I think about gold, but gold is always going to remain the safety that for any investor in the world. And at the end of the day, if M and A… And M and A usually is interesting. When gold price goes up and then M and A goes up. In reality, M and A should be strong when he price of gold is lower because it’s cheaper, but people are worried. So they just start buying only when the gold goes up. My job is to create value for shareholders. I personally, our family owns, 5.3 million share of Gold Terra.

We are very excited about working in Canada, in Yellowknife, with infrastructure. We don’t have to bring people in. Everybody goes home at night. It’s very, very important. And the cost of underground mining when you’re already in town is a lot better than going in 200 or 300 kilometers away from town. You think about… I still remember building Detour and being compared with Canadian Malartic and Osisko. And I could never come up with the same numbers as Osisko because Osisko is in town. Everybody goes on at night. It’s such an advantage. Nobody realize how important it is, to be in town. So the… I think 3 million ounces in a town… It will be a very good and nice achievement and maybe more, I think I’m very open to find a lot more because of our land position and because of potential that lies in the Campbell Shear and what has been done. So remember, 14 million ounces produced so far and the Campbell Shear is open North and South.

from Kerry Lutz Podcasts – Financial Survival Network https://ift.tt/3oPiowv

Today the man who has become legendary for his predictions on QE and historic moves in currencies and metals told King World News that the global population will be cut in half as financial and economic chaos erupts.

We spoke with Ivan Bebek Co-Founder/Co-Chair/Director and Peter Dembicki President/CEO of Tier One Silver, particularly about it’s impending listing on the TSX-V. (TSLV). It could come as soon as this Thursday. US Investors will be able to purchase shares through brokers that allow purchase of Canadian stocks, such as TD Ameritrade, Charles Schwab, Interactive Investors and others. The US listing will come within a matter of weeks.

Originally Bebek was planning for a February listing. The Venture Exchange has been backlogged with numerous mining companies who are working through the listing process. Delays are frustrating, but here it will eventually work to Tier One investors’ advantage. Once the drill starts turning and results follow, few will have any memory of the delay.

More importantly, while pursuing the listing, management has been extremely active. A major acquisition was consumated and more studies of the Curibaya Project were conducted in an effort to develop new targets. Additional samples were done and robust numbers returned. Bebek says that the company is now in a very strong position to develop multiple projects.

CEO Dembicki observed that permits are in place and drilling will start in just a few short weeks. Peruvian assay times are relatively rapid, so expect results and news-flow to come fast and furious. And companies are once again getting paid a big premium for major discoveries. That could mean huge outsized returns for shareholders, such as yours truly.

Peter Boockvar: Chief Investment Officer of Bleakley Financial Group - In his role as Chief Investment Officer, Peter leads the team that is responsible for the development, management and oversight of Bleakley’s investment management program, managing the investment committee, and setting the firm’s overall investment philosophy, global investment outlook and asset allocation decisions. Peter also...

Peter Boockvar: Chief Investment Officer of Bleakley Financial Group - In his role as Chief Investment Officer, Peter leads the team that is responsible for the development, management and oversight of Bleakley’s investment management program, managing the investment committee, and setting the firm’s overall investment philosophy, global investment outlook and asset allocation decisions. Peter also...

For more than 20 years, Master Trader Nick Santiago has been beating the markets. He’s made some incredible calls along the way and now he’s looking to spread the word. There’s no reason that the average trader should be coming up short. So now we’ve started a daily show to bring you up to date on the latest market developments. Nick will be sharing trades and concepts and discussing current trends.

Trilogy Metals (Tickers – TSX/NYSE-MKT: TMQ) (sponsor) has been ceaselessly working to develop Alaska’s Ambler mining district, which has a huge high grade copper deposit of over 4%, along with larges amounts of gold, silver, lead and zinc. They’re benefitting greatly from record high copper prices. The company is extremely well capitalized, with over $80mm in liquidity and a major joint venture partner South 32. We got an update from President/CEO Tony Giardini. He’s got 15000 meters of drilling planned for this year, financed by a huge $27mm budget.

We asked Tony what affect high copper and gold prices will have on the latest FS (feasibility study). The answer is quite substantial, he indicated that the NPV (net present value) had nearly doubled to $2 billion and it’s IRR (internal rate of return) was over 40%.

We also got a status update on the road that will connect the company’s projects to the famed Dawson Highway. It’s all systems go. The state agencies and the company have budgeted funds to get work started and all interested parties are working hard behind the scenes to make this project a reality. And TMQ’s share price has responded accordingly, recently making new 52 week highs, nearly double it’s 52 week low.

While this is a longer term project, its success is greatly enhanced by the world’s insatiable demand for copper. In the transition to an electrified future, Trilogy will play a vital role.

Sign up (on the right side) for the free weekly newsletter.

from Kerry Lutz Podcasts – Financial Survival Network https://ift.tt/3u2WKpG

Master Prepper Dunagun Kaiser discusses Financial Prepping and why you need to get started now, if you haven’t already. It all comes down to the individual, you can’t expect the government to suddenly come to its senses and start doing the right thing. They’ve forgotten the fact that they are public servants and there to further the common good. The Marxist Agenda is alive and well. Vast numbers of people have become wards of the state. We just went through Tax Day, we’ve become indentured servants of the state. Anything we can do individually to reduce our tax burden and the power of our leaders. People are continuing to vote with their feet. Andy Schectman, Lobo Tigre and many other that we know are fleeing these progressive jurisdictions. Freedom loving states are changing things for the better. Make the decision to stand up for your freedoms and if that means moving, so be it.

For more than 20 years, Master Trader Nick Santiago has been beating the markets. He’s made some incredible calls along the way and now he’s looking to spread the word. There’s no reason that the average trader should be coming up short. So now we’ve started a daily show to bring you up to date on the latest market developments. Nick will be sharing trades and concepts and discussing current trends.

First on the agenda, are cryptos a magical creation exempt from all the known market forces? David Morgan believes that Fibonacci will have his revenge. A major retracement is inevitable. Then we discussed his open letter to Elon Musk, urging him to buy silver. Our solar clean energy future depends upon it. There’s not enough silver in the world to switch over to solar and green, but that won’t stop the dreamers. Solar panels only last for 10 years and then need to be replaced. Windmills aren’t lasting the 20 years as expected. Social media has distorted reality and brainwashed the masses. Everything nowadays is based upon emotion. Under the current technological conditions our green energy future isn’t going to happen now or in the future. Just wait for precious metals to realize their true value.

For more than 20 years, Master Trader Nick Santiago has been beating the markets. He’s made some incredible calls along the way and now he’s looking to spread the word. There’s no reason that the average trader should be coming up short. So now we’ve started a daily show to bring you up to date on the latest market developments. Nick will be sharing trades and concepts and discussing current trends.

Dr. Michael Busler returns to the program… The 1970’s are back, complete with inflation, gas lines, and presidential fiddling. Inflation in April accelerated at its fastest pace in more than 12 years as the U.S. economic recovery kicked into gear and energy prices jumped higher, the Labor Department reported Wednesday. The Consumer Price Index, which measures a basket of goods as well as energy and housing costs, rose 4.2% from a year earlier. A Dow Jones survey had expected a 3.6% increase. The month-to-month gain was 0.8%, against the expected 0.2%.

Gold and silver breakouts are everywhere as the metals markets continue to catch a bid. One of the greats in the business said, "We've waited a long time for this."

John Rubino is back… Musk’s crypto conflicts, don’t fall in love with a 9 year old, Elon Musk. Did Tesla sell its Bitcoin? Is this insider trading? What does it mean for cryptos? Hot money likes it and will leave as quick as it came. This is what happens in a bubble. Time to stop HODLING? Michael Burry reveals a huge short in Tesla. Sam Zell is also on the same side of trade. Gold likes Basel III, is it the death knell of the LBMA. The big banks have been able to lie about the value of the futures contracts on their books, which means they’re worth nothing. The big bullion banks are threatening to leave the paper market. This would lead to physical valuation rather than paper valuation. The World Economic Forum has cancelled its 2021 annual meeting scheduled for Singapore in three months time, the Swiss-based organisation said on Monday. The next annual meeting will instead take place in the first half of 2022. … Speculative assets falling out of favor SPACS, NFTs, Reddit stocks, cryptos while money flows into safe havens like precious metals … They’ve all failed. This is how bubbles work? Will big Tech stocks be next? Remember the 1990’s when the land under the Imperial Palace in Japan was worth than all of Manhattan’s Real Estate. Covid is now almost officially gone. It’s under 5% of deaths which means it’s no longer considered an epidemic. And against all odds, masks are starting to fade into memory, at least in some places like Florida and Texas.

Sign up (on the right side) for the free weekly newsletter.

from Kerry Lutz Podcasts – Financial Survival Network https://ift.tt/3hAxRiu

For more than 20 years, Master Trader Nick Santiago has been beating the markets. He’s made some incredible calls along the way and now he’s looking to spread the word. There’s no reason that the average trader should be coming up short. So now we’ve started a daily show to bring you up to date on the latest market developments. Nick will be sharing trades and concepts and discussing current trends.

One of our favorite things is bringing you good news from a sponsor. And lately Doré Copper (TSXV: DCMC – OTCQB:DRCMF) has had a lot of really good news. What you’re about to hear is hot off the press. Doré’s 2020 and recent 2021 drill programs have hit the mark. The plan was well thought-out and meticulously executed. CEO Ernie Mast believes he’s very near his goal of a 5 million ton resource, a whopping 65% increase over over Doré’s 2019 43-101 estimate. These results reinforce that Corner Bay is the cornerstone asset of Doré’s holdings. Ernie is delivering exactly what he promised; the hub-and-spoke concept appears to be a winner both for Dore and its shareholders (including us).

Alasdair MacLeod writes, “Basel 3 is on course to regulate the LBMA out of existence. And with it will go all the associated arbitrage business and position-taking on Comex, because most bullion bank trading desks will cease to exist. The only supply to buy-side speculators of gold and silver contracts will be producer hedging.” In other words the gig is up and the Emperor has no Gold. You heard it here first.

Today the man who has become legendary for his predictions on QE and historic moves in currencies and metals told King World News that a global financial fire is coming and investors must get prepared now.

Trillium Gold Mines (TSX.V:TGM — OTCQX:TGLDF) CEO Russell Starr is always in search of value, which explains why he’s been buying shares in his own company, Trillium Gold (sponsor). He stated, “It doesn’t get much cheaper than Trillium.” In the longer term, he believes that value always wins out.

At present the company has two drills turning and is in the process of adding a third. It’s awaiting the assay results from 5000 meters of core. Russell is frustrated by the assay lab backlog that has plagued the industry with lengthy delays. However, he expects the release of Trillium’s drill results to be imminent and that the stage is set for the Newman Todd Project to deliver some excellent numbers..

It is often said that management may have many reason to sell its shares, but it only has one reason for buying them. As shareholders we believe this will hold true for Trillium.

Sign up (on the right side) for the free weekly newsletter.

from Kerry Lutz Podcasts – Financial Survival Network https://ift.tt/3olbBuh

James Turk: Founder & Lead Director of Goldmoney, Inc (Toronto Exchange XAU) - His latest venture is Lend & Borrow Trust Company Ltd., an online peer-to-peer lending platform that brings lenders and borrowers together by enabling customers to borrow CAD, USD, GBP, EUR or CHF using their gold and silver as collateral for security to the lender...

James Turk: Founder & Lead Director of Goldmoney, Inc (Toronto Exchange XAU) - His latest venture is Lend & Borrow Trust Company Ltd., an online peer-to-peer lending platform that brings lenders and borrowers together by enabling customers to borrow CAD, USD, GBP, EUR or CHF using their gold and silver as collateral for security to the lender...

Fury Gold Mines (Ticker:FURY) CEO Michael Timmins and Chairman Ivan Bebek provide an overview and update on the company’s progress. Michael commented on the advancement at Fury’s flagship project: “Eau Claire continues to impress us. And I think it’s the sheer scale of the mineral endowment that has surprised us the most. This is the type of project that I was searching for back when I was at Agnico Eagle. Significant growth, high-grade gold, easy access, gold at all project scales and in different geologies and the suite of regional targets, that’s going to offer that long-term growth.”

Ivan commented on why he is excited about Fury Gold’s potential: “Just a tremendous amount of deep value. And just listening to Mike, talk about the projects and what’s on deck and coming, it reminds me of why I want to own a lot more of Fury, when appropriate. We have a lot of results pending, so I’m going to wait until they’re all out, but I just feel there’s a tremendous amount of deep value behind this robust exploration and all the torque you look for as a shareholder. And I think that’s going to be lived every month for the rest of the year. There’ll be some holes to look for that could really, really change the game for us considerably, to the upside. Love the direction the company’s headed. Feel it’s a tremendous opportunity right now. I don’t know the results yet. Obviously, want to know them as much as everybody listening, but there’s enough holes there that can give us a lot of different ways to win for investors. Not just here. There’ll be the ones at Homestake as well as at my favorite, Committee Bay, this summer. So, I look forward to an extremely active year. Company’s busy and you’re going to hear a lot from Mike and the team.”

Sign up (on the right side) for the free weekly newsletter.

0:00 Introduction

1:37 Eau Claire project overview

4:20 Gold macro situation & Fury Gold’s valuation

8:43 Shelf prospectus & why Fury filed it

10:34 Ivan’s perspective on flow-through financing

12:12 High-grade gold in Canada

15:00 Drilling focus among three projects

18:50 Upcoming catalysts

TRANSCRIPT:

Bill: Joining me today is Mike Timmins, the president and CEO, as well as Ivan Bebek, the chairman. Gentlemen, welcome to the show. Mike, I’m going to kick it over to you first. Can you kind of remind us of what the goals here are at your flagship project and what progress have you made thus far?

Mike: Yeah. Thank you, Bill. We’re happy to be here and I’m glad Ivan is here too. It’s good for a chairman to come in. Talk a little bit about the view from that seat and also as one of our major shareholders, so thank you to him, for joining us. We’ve been very busy, Bill at Eau Claire, obviously drilling the deposit and stepping on along the various extensions, as you’ve seen in the notes. The new Snake Lake structure that we’ve identified, which is parallel to Eau Claire, can be a step change for the project.

So, we’re hitting Snake Lake in behind our step-out drilling of Eau Claire, over a kilometer away from its surface expression. So, we’re actually developing a view that that might have the same size potential as Eau Claire itself. It is early days. Results out this month on our first three step-out holes below Snake Lake. So, that’s a pretty exciting development for us. The 850 Zone hosts Eau Claire’s western extensions. The previous owners were really focused on shallow open pit material and completely missed the Eau Claire potential which lies at about 300, 400 meters below that.

So, this has huge potential to add ounces, literally in our basement, within the original PEA footprint. So, another big eye-opener for us. We’ve also been very successful, I think, at deriving regional targets by diving deep into the data. A comprehensive review of the geophysics simply hadn’t been done before. And we recognize this incredible opportunity doing the due diligence, of really just starting to see those results coming out now of that work. Eau Claire continues to impress us. And I think it’s the sheer scale of the mineral endowment that has surprised us the most. This is the type of project that I was searching for back when I was at Agnico Eagle. Significant growth, high-grade gold, easy access, gold at all project scales and in different geologies and the suite of regional targets, that’s going to offer that long-term growth. And as you pointed out where we are, 20,000 meters into the first 50,000 meters program, and I’ve already outlined a ton of potential. And as you know, Bill, we’re just getting started.

Bill: So, with this Snake Lake target, if you’re successful there, are we looking at a big open pit or would this be like a satellite pit? I know you’re at the conceptual level now, but can you give us a taste of what this might mean, if you’re successful there?

Mike: It would be pit and underground, the same thing as Eau Claire, but we’re hoping it’s a mirror of it, is the big goal.

Bill: Okay. Ivan, could you kind of speak to the valuation and the macro situation? I was chatting with Mike before we hit record and I said, “You’ve had nothing but headwinds. Since he took over, the gold price goes from above $2,000 down below 1700. Now we’re trading sideways. So, the gold price hasn’t been helping. What is your analysis of the macro situation in the gold sector and specifically, Fury’s valuation right now?

Ivan: Okay. First off, great to be back here. Mike and his team have been doing an amazing job. Something that you don’t see that happens in our groups and specifically with Fury, is you don’t see the work behind the scenes that makes all of this happen. It’s really fun to point to great drill holes. It’s really fun to come out with a great plan, but executing that is paramount. And Mike’s really made it feel like we work with Agnico Eagle here, based on a lot of the professionalism that he’s brought across every platform in the company. So, hats off to Mike there. This doesn’t pay you today, shareholders, but it will pay you tomorrow. It will gander us a big premium later down the road, once things really start to come together for us.

And to your comment or your question about the headwinds, we don’t like excuses. We like results. And we like to show performance for our shareholders, but it has been challenging. And I’ve done this for about 21 years. And since we came public, gold went down almost $300 an ounce and we hit the worst sentiments since ’01. And when you can’t get love in the market, you just make sure you’re working really hard to create those opportunities for shareholders, going forward.

And you just heard Mike, talk a little bit about the holes at Snake Lake, something called the 850 Zone. There’s some big areas to really… And I like the word step change… Or a game changer would be the more familiar word… But step change is a word I like even better… The actual projects to double that potentially or triple it in size, which is something we felt originally had huge potential at Eau Claire. And that is where we’ve been heading, is in that direction. We have a great handle on the deposit. On the macro part of the gold market, I think we’ve seen a turn. We’ve seen it bottom pretty bad through a really tough quarter last quarter.

And I think the second half of the year, if you listen to many of the experts and see the money flow starting to come back to the space, I think we’re going to see new highs in gold. And when you look at that and think about Fury has 3.7 million ounces of seven grams per ton gold as an average grade just over seven grams. That’s a big statement. Not many companies have that, of our size and not many companies are able to find that anymore, because the exploration has gotten so much more difficult.

So, from that perspective, I think that all the hard work we’ve done and we’ve worked hard and Mike, I think you’ve had about three, 400 Zoom meetings. You know, Mike’s relentless. He doesn’t stop, because we have something to say. And this, I think is going to equate to us going from being with our peer group to performing well past the peer group. And what’s really going to do it and what does it for me every day. Is when I hear big exploration targets. I was a bit concerned at Eau Claire that there wasn’t that huge Committee Bay look to it or that huge upside look. I knew it could be there, but I needed to see more.

And Michael Hendricks and the team and Brian Atkinson, and the guys, have really done a phenomenal job of sifting through the copious amounts of data and something… And Mike Timmins, maybe you can comment on this. I’ve heard there’s a huge amount more samples that were not worth being used by our predecessors within the region on the project. And they’re getting to a lot better concepts for some big swings to take this summer too. So, I think for me, that’s a huge compliment on the project.

Mike: That’s true. I mean we are finding more data as we go and as we dig. As we round up the computers at camp and everything else and correlate it, so that we have one consistent systematic geological picture. So, that’s a 100% correct.

Ivan: Yeah. And then just the pace we’ve been going at, Bill. We’ve never slowed down. You know, bad market, some people become a little bit apprehensive about the pace they’re going at, but the confidence in the project goes up, you move forward. And if you believe in the gold market, you know that’s going to continue. You really step into your projects and that’s what we’re doing here. So, no, it’s been a lot busier than the share price would reflect. And I think that, in the next, as Mike said, six weeks, you’re going to start to see all of those results from all of this heavy lifting that we’ve been doing. In the second half of the year here, we should turn the corner with a lot more gold to talk about. And other programs that are on the horizon.

Bill: Ivan, you put out a press release recently about a shelf prospectus. Can you explain to listeners what that is and how you intend to raise money, moving forward?

Ivan: Sure. Shelf is a very, very, very efficient way of raising capital. There’s a bit of head cost, upfront, but we can raise up to $200 million in using this mechanism called the base shelf. And basically, if we want money in a week from now, we can get money in a week from now. I mean, if we’re marketing, if there’s investors interested that want to participate in a funding or in a large block of shares, we can close the transaction within one week. Now, traditional bought deals take about 45, 50 days, including the marketing that goes around and the legal costs can be astounding at times. And we all know that gold is volatile. The market is cyclical, but this gives us speed to capital. This also takes away the need to require to do a big funding, like a $20 million funding at once or a 30.

This gives us the chance to do five million here, 7 million there, and be very, very strategic with how we raise capital. So, we don’t ever have a big burden of a heavy financing to worry about. Right now, we’re in good shape financially. I think March 31st, we had about 10, $11 million in cash. And so, we don’t need money yet. We’re going to need it throughout the year, but small fundings along the way, unless we see a very, very key shareholder we want to add to the registry, an institution or an investor of consequence, we’d always consider that. But it allows us to be more strategic and a lot more inter dilutive with our financing approach.

So, it’s a big thing. We’re going to actually do this in all the companies I’m involved in, for the same purpose. One week to get the capital and to pick your shareholders carefully, as that’s been the real, real big important part of our culture and our share structures. It allows us to do that better.

Bill: Because your key project is in Quebec, what’s your take on flow-through financing Ivan? There’re pros and cons to it. And because you’re so particular of who you bring into the stock, sometimes you can bring in people that will sell the stock sooner than later, if you do a flow-through, even though you raise at a premium. What’s your take?

Ivan: So, we’ve done only charity flow-through. All of our money that we’ve raised at Auryn and all the money we’ve raised here, which is a lot different from flow. What charity flow-through is, it’s a mechanism where the buyer can be anybody. It can be an American. It can be a Canadian. It can be somebody overseas. But we get a premium on the price they pay when they make the investment. The only thing negative about charity flow-through, it’s not always available. And then on straight flow-through itself, which you asked me about, it’s something that I’ve turned away from because investors are not as aligned with the business of the company. They’re more aligned with the business of a tax saving transaction for their personal taxes.

So, from us, I think you would only see charity flow-through at the very best, but you know, it’s not available in huge capacities at all times through the year. And if you want to do a program and raise $5 million and there’s no flow-through available, we might have to do hard dollars. And we’re okay with that, because we might be able to do that on the back of some great results and pick better prices due to the one week, start to close, completing one of those transactions. So, either way, I would say it’s a benefit, because you can raise money at 80% premium to your spot price. Now that’s roughly where it ends up in Quebec. Or 40, 45% premium in Committee Bay or Homestake, but it’s not always there. We’ll use it when we can. And we’ll just make sure that we’re not doing the traditional flow-through where we don’t have control of the investors.

Bill: Mike, you have three projects in Canada. They are high-grade. Remind listeners, again, the focus of the company in terms of being in Canada and pursuing high-grade gold.

Mike: Yeah. I think there are many benefits to focusing on high-grade. So, you’ve got robust project [inaudible 00:11:46] clinics. You’ve got high-grade deposits, are exciting to drill at any gold price. So, you can be at 1250 or 2,500 and you’re still putting out high-grade gold. So, it’s exciting. And so, it weathers that storm. Investors looking for low risk in the mining sector can often filter on grade. And so, if they filter on high-grade, there’s only going to be a few names. And Fury, obviously stands out from the crowd. Drilling and growing high-grade gold deposits is challenging to say the least. Mother Earth is not easy. And so, the goal is to keep the rest of the business as low risk as possible.

So, we have very limited social risk. Low financial risks, now that we’ve put this prospectus in place, as Ivan has talked about. We have low execution risk, with great infrastructure at all three of our projects. And I think the same goes for Canada. If you really look at it, we enjoy the rule of law. There’s a clear permitting pathway for mineral development in every province and every territory. I think even more important is the fact that a lot of rural or remote communities have mining experience and knowledge, which provides comfort for them and ease of business for us. And again, I’ll use an Agnico Eagle reference. They’ve kept their business manageable and the strategy simple for decades, by focusing on grade and staying in stable jurisdictions, and Fury is no different.

Ivan: I just want to add one thing there Bill, on the high-grade and grade is king, as Mike really eloquently put together for us and why. High-grade is also variable. So, you’re going to see holes that come out. You’re going to see some narrow. You’re going to see some wide. You’re going to see a combination. What you can look at is companies like Kirkland Lake. It did phenomenal with its high-grade portfolio of projects. The profitability was astounding. Cisco, as well, in Quebec, not long ago. They were doing extremely well with their project, but it required a lot of drilling.

So, there’s a good chance we will require a lot of drilling, because we’re seeing a lot of high-grade. Or there’s a good chance we’re going to see variability through our drill results. As long as we’re hitting gold and as long as we’re hitting high-grade, then everything that we’ve set out to do with Eau Claire is going to be on full cylinders going forward. So, from my perspective, I think we’ve got a lot of it to start with and we’re going to have a lot of it to work with, in the coming months.

Bill: So, Ivan and Mike, whoever wants to answer this question, please jump in. Seven months ago, when we talked about Fury Gold and we were laying out the vision, we said, 80,000 meters over the next 18 months. 50,000, were going to be at Eau Claire. But Ivan, you’ve also said that Committee Bay is a gold bull market project, so you’re going to be sensitive to that. Are we going to take any of the meterage from like a Committee Bay and maybe put that more at Eau Claire? Has that shifted at all in how you guys are spending these dollars that you’ve earmarked for this?

Mike: Yeah, sure. Bill, I think it all depends on the results. I mean, as you said, we’ve just really gotten started at Eau Claire. And so, what we want to do is we want to come full circle on some of the concepts that we have there. Both, what is Snake Lake? What it will ultimately be. We’re not done with one kilometer down punch extension yet. What are we seeing out West? I mean, those results have to come out. That will resonate. There’s Homestake Ridge, which we haven’t discussed either. We put plans out for Homestake. We put plans out for Committee Bay. Those are subject to planning, going forward. The 80 to a 100,000 meters that we’ve kind of socialized and suggested that we’re going to do over the next 18 months is across the entire platform.

But of course, you do it one step at a time because we’re disciplined. We said, we want to know as early as possible, how big Eau Claire can get. Can we go from 80,000 ounces a year that was in the PEA to something in the ground that can support 150 to 200,000 ounces of production per year? That first junior producer category. Can Eau Claire, do that? I think it can. So, it’s a matter of, it’s a matter of just… It’s chapter one, chapter two, chapter three. Just move through it. And then we’ll make decisions, obviously, as a group, together with our board, as to where we want to allocate meterage. Where we want to allocate our budget.

Ivan: And actually a good point here, Bill to your comment about the shelf. And that allows us to raise money in June, from Homestake or end of may. And raise money in July for Committee Bay. We don’t need to raise all the money today, which normally would put a damper on the share price. And, fortunately, I think we have six or seven holes that we are really, really keen on the results from, to come out here in the next three to six weeks, as Mike’s put out.

And, if that works with us in currency, the goal would not be to take away from any project. It would be to add to each project. We’re going to be aggressive. And so, I like Mike’s answer because it’s very true. We’re going to be careful with what the results tell us what to do, on the projects we haven’t started drilling yet. Now the good news is we’ve done all the work, so they’re ready to drill. We’re in the position to do that. And that was the press release the other day, the corporate update. It was letting everybody know how busy we’ve been, how organized we really are, but we’re actually ready to go.

And so, a little bit of wind from the gold market and some great results out of Eau Claire puts us in a position to raise a lot more capital than we need to do the rest of these projects and maybe move that 80,000 number up, which would be my preference, just because I want to go for it on all levels. And I really, really believe in this gold market. And so, I think the other comment that as we’re talking here resonates with me, is I feel there’s been a big miss. There’s a massive miss.

And if you look at the results on Eau Claire today, if you look at the grade we’ve hit, if you look at the steady, there’s always been something new being added, incremental increases and whatnot. We are increasing our understanding. We are liking the project more than we first had it. And now, there’s a big regional picture that Mike alluded to, that we’re going to deal with this summer, but it really is a chance to be a real district. And I think for me, it’s something that’s performing internally and we hope to see it in the share price soon.

Bill: Mike, you’ve taken a multi-year, long-term perspective on building value, but speculators like myself, we get impatient and it becomes more, “What have you done for me lately?” So, could you just remind us what’s on tap over the next couple of months? What catalyst should we be looking for?

Mike: So, at Eau Claire, I think it’s Snake Lake and the 850 Zone drill results are going to be the big catalyst this spring, as we continue to execute and demonstrate the project’s growth potential. That’s just ongoing. That’s going to be coming. Assuming continued success and we’re all assuming it, you could expect another drill or two to go to Eau Claire, which is obviously going to dramatically increase our capabilities there and the rate of news coming out to the market. This summer at Eau Claire, we’re going to be developing eight new, regional target centers that Ivan just spoke about. Bring them all to the drill stage and set up to drill into fresh rock.

Any one of those targets could be that next new major bull discovered. So, that’s exciting. Another near-term catalyst for us could be the commencement of drilling Homestake. And we’ve talked about that already. We are very excited with our plans for the project and I would expect a great deal of value to be translated into share price. It would show people all of the good things that can happen when you’re drilling high-grade gold [inaudible 00:19:31]. So, a big year planned for investors in 2021, Bill.

Bill: Ivan, final thoughts?

Ivan: Just a tremendous amount of deep value. And just listening to Mike, talk about the projects and what’s on deck and coming, it reminds me of why I want to own a lot more of Fury, when appropriate. We have a lot of results pending, so I’m going to wait until they’re all out, but I just feel there’s a tremendous amount of deep value behind this robust exploration and all the torque you look for as a shareholder. And I think that’s going to be lived every month for the rest of the year. There’ll be some holes to look for that could really, really change the game for us considerably, to the upside. Love the direction the company’s headed. Feel it’s a tremendous opportunity right now. I don’t know the results yet. Obviously, want to know them as much as everybody listening, but there’s enough holes there that can give us a lot of different ways to win for investors. Not just here. There’ll be the ones at Homestake as well as at my favorite, Committee Bay, this summer. So, I look forward to an extremely active year. Company’s busy and you’re going to hear a lot from Mike and the team.

from Kerry Lutz Podcasts – Financial Survival Network https://ift.tt/2SLyYBr